Financial Freedom Within Reach: Strategic Savings Can Tackle Significant Debt

A recent financial consultation highlighted a powerful truth: even with substantial debt and no retirement savings, individuals can chart a course towards financial stability by making controlled, strategic adjustments. The case of one individual, identified as Ann, facing $41,000 in debt and significant monthly expenses, demonstrates how decisive action on controllable costs can dramatically accelerate debt repayment and improve financial well-being.

Analyzing the Debt and Expenses

Ann’s financial picture revealed a substantial car payment of $450 per month, on a vehicle valued at approximately $16,000 (a 2022 model). This car debt alone represented a significant drain on her monthly income, leaving little room for savings or debt reduction. Furthermore, her housing situation involved a three-bedroom, one-bathroom home with a lease set to expire in April. While the total rent was not explicitly stated, the implication was that her individual share was high, as the consultant advised that a three-bedroom home is unnecessary for someone living alone unless roommates are involved.

The Power of Controlled Spending

The core of the financial strategy focused on Ann’s ability to control two major expenses: her vehicle and her housing. The consultant proposed a two-pronged approach:

- Vehicle Optimization: Selling the current 2022 vehicle and purchasing a cheaper, more affordable car was identified as a key step. The $450 monthly car payment, when eliminated, would effectively act as a $5,400 annual raise. The initial homework assignment was to determine the car’s market value using resources like Kelley Blue Book to facilitate a sale.

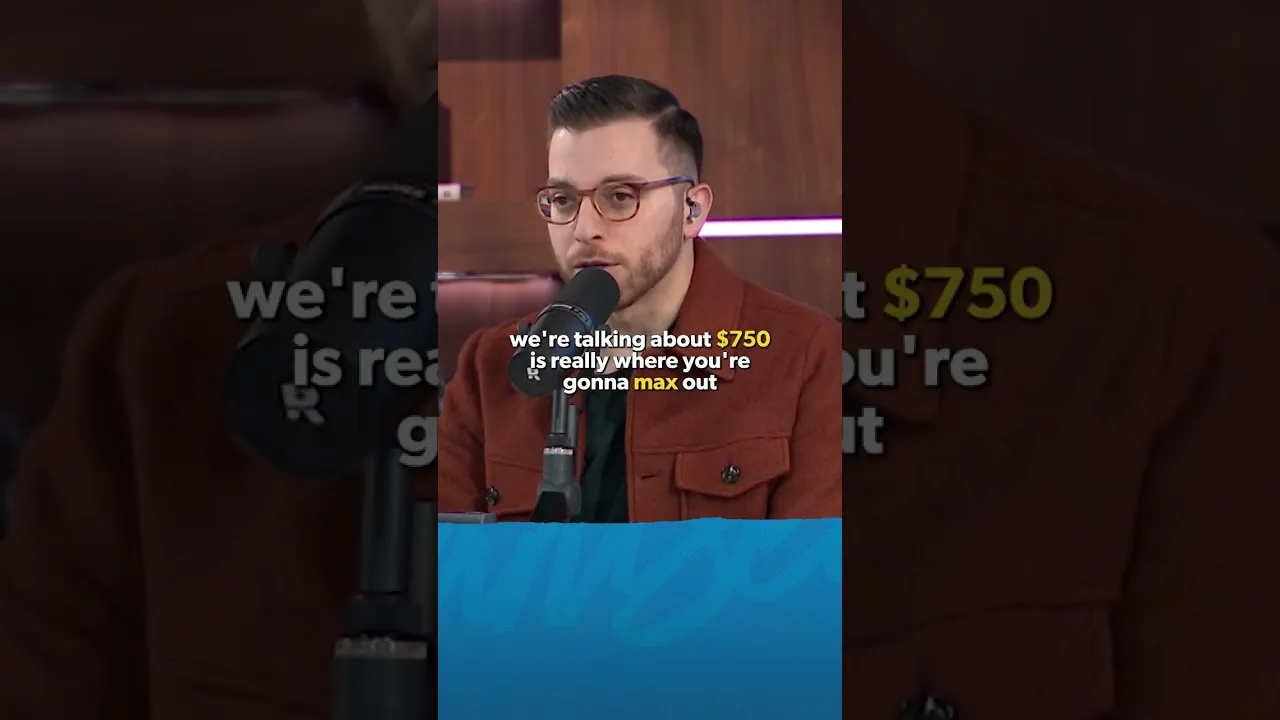

- Housing Adjustment: The existing housing arrangement, a three-bedroom home, was deemed excessive for an individual. The recommendation was to secure roommates to share the living space. This move was projected to significantly reduce her monthly housing costs. The target for housing expenses was set at a maximum of 25% of after-tax monthly income, equating to about $750. By bringing in roommates, it was estimated that Ann could cut her share of the rent by approximately $1,000 per month.

Quantifying the Savings and Debt Payoff

The impact of these two adjustments is profound:

By selling the car and securing roommates, Ann could potentially free up $1,500 in extra cash flow each month. This is achieved by eliminating the $450 car payment and cutting her rent by an estimated $1,000.

This newly found $1,500 per month in available funds could be directly applied to her $41,000 debt. At this accelerated payment rate, the entire debt of $41,000 could be paid off in just 27 months ($41,000 / $1,500 per month ≈ 27.3 months).

What Investors Should Know

While this scenario focuses on an individual’s personal finances, the underlying principles resonate with broader market dynamics and investor psychology. The ability to identify and control variables within one’s financial life is crucial for achieving financial goals, much like investors must manage risk and allocate capital strategically.

- Discretionary vs. Non-Discretionary Spending: The case highlights the difference between essential spending and discretionary spending that can be optimized. For investors, this translates to understanding which expenses are fixed and which can be adjusted to increase savings or investment capital.

- Debt Management as an Investment Strategy: Aggressively paying down high-interest debt can be viewed as a guaranteed return on investment, often exceeding what can be reliably earned in the market. Eliminating debt removes financial drag and frees up capital for wealth-building activities.

- Behavioral Finance: The psychological aspect of feeling “stuck” due to perceived immovable expenses (like a car payment or rent) is a common challenge. Overcoming this requires a shift in perspective, recognizing that even significant expenses are often the result of choices that can be re-evaluated and changed. This behavioral shift is key for both personal financial success and disciplined investing.

- Long-Term Implications: Successfully navigating such a debt-reduction plan not only frees up significant capital but also instills financial discipline. This newfound discipline can be channeled into consistent saving and investing, paving the way for long-term wealth accumulation and retirement security, even from a starting point of having “nothing saved.” The example emphasizes that it is never too late to change financial trajectory with focused effort.

The core message is that by taking control of controllable expenses, individuals can create substantial financial momentum. The ability to generate an extra $1,500 per month through strategic adjustments to car ownership and housing can transform a daunting $41,000 debt from a decades-long burden into a manageable two-year payoff plan, setting a foundation for future financial health.

Source: She's 50 with Nothing Saved for Retirement (Part 2) (YouTube)