401(k) Founder’s Warning: Retirement Crisis Looms

The very person who created the 401(k) retirement savings plan now regrets it. Ted Benner, the architect of the 401(k), has called his creation a “monster.” He believes people have misunderstood its purpose, treating it as their sole retirement fund. This misunderstanding, he fears, is a major reason for the current retirement crisis facing millions of Americans.

“If I were starting over from scratch today with what we know, I’d blow up the existing structure and start over.”

Benner’s regret stems from the widespread belief that a 401(k) combined with owning a home is enough for a secure retirement. Sadly, data suggests this is not the case. The current retirement crisis highlights that this two-pronged approach is statistically insufficient for many.

The Shift from Pensions to 401(k)s

The retirement landscape has dramatically changed. In the early 1980s, when the 401(k) emerged, about 60% of Americans relied on pensions for retirement income. Pensions placed the financial risk on employers, who had to ensure funds for retirees. Companies then introduced the 401(k) as an alternative. This shifted the responsibility of saving and investing entirely onto the individual employee.

Today, only about 15% of Americans have access to a pension. Most now depend on 401(k)s. The original intention of the 401(k) was to supplement, not replace, other retirement income sources like pensions, Social Security, and personal savings. It was meant to provide extra comfort for a more comfortable retirement, not to be the entire retirement plan.

Hidden Costs Eroding Your Savings

Many people are unaware that their 401(k) accounts come with fees. In fact, 70% of Americans don’t know they are paying fees within their 401(k). These fees are charged by money managers who handle the investments. They take a percentage of your invested money and any profits earned each year.

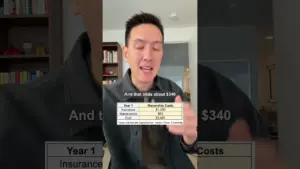

The problem isn’t paying for a service, but rather overpaying without realizing it. This can significantly reduce your long-term gains. Consider this example: Investing $500 monthly for 30 years with a 7% annual return.

- With a 0.5% annual fee, you could retire with approximately $474,000.

- However, with a 1.5% annual fee, your retirement nest egg shrinks to about $377,000.

That’s a difference of nearly $100,000 lost to higher fees. These fees are often called “expense ratios.” The average expense ratio for 401(k) accounts under $1 million in the U.S. is currently 1.26%. Investors are urged to check their expense ratios, as high fees combined with underperforming investments can severely hinder wealth accumulation.

Understanding Your Tax Options: Traditional vs. Roth 401(k)

401(k)s are known as “tax-advantaged” accounts. This means you get a tax benefit, but you still pay taxes eventually. The key difference lies in *when* you pay them, depending on whether you choose a Traditional or Roth 401(k).

- Traditional 401(k): You contribute pre-tax money. Taxes are deferred until you withdraw the money in retirement. The argument is that your tax rate will be lower in retirement when you have less income. However, future tax laws are uncertain, and national debt could lead to higher tax rates.

- Roth 401(k): You contribute after-tax money. Your investments grow tax-free, and qualified withdrawals in retirement are also tax-free. This is beneficial if you expect your tax rate to be higher in the future or if you aim to build significant wealth that generates higher income in retirement.

The choice depends on your current income, expected future income, and predictions about future tax rates.

The Stark Reality of Retirement Savings

To live a comfortable retirement, many experts suggest needing around $1.5 million. However, the average 401(k) balance in the U.S. is currently about $146,000. This is less than a tenth of the commonly cited retirement goal.

Looking at the median balance offers a clearer picture. The median 401(k) account holds just $38,176. This figure shows that most Americans are significantly short of their retirement savings goals.

Generational data reveals the gap:

- Baby Boomers (closest to retirement): Average of under $250,000.

- Gen X: Average of $192,000.

- Millennials: Average of $67,000.

- Gen Z: Average of $13,500.

These numbers underscore the severity of the retirement crisis. Many individuals face the prospect of insufficient funds, potentially needing to work longer or rely heavily on Social Security, which may not be enough.

Actionable Steps for a Secure Financial Future

Given these challenges, proactive financial planning is essential. A key principle is managing your money effectively by following a disciplined approach to spending, saving, and investing. For instance, a 75/15/10 rule suggests spending no more than 75% of your income, investing at least 15%, and saving at least 10% for emergencies.

The focus should be on *where* and *how* you invest. The traditional advice is to follow the 4% rule: If you need $60,000 per year in retirement income, you’ll need $1.5 million saved ($60,000 / 0.04). This requires your investments to grow effectively.

Ultimately, financial freedom, not just traditional retirement, should be the goal. This means building assets that can either be sold for a lump sum or generate ongoing income. Wealth is defined by having assets that pay you, not just by earning a salary.

Optimizing Your Investments

The speed at which you build wealth is determined by your investment returns. While the average stock market return has historically been around 10% per year, many 401(k) accounts fail to achieve this due to high fees and underperforming funds. Low returns combined with high fees result in even slower growth.

By improving your investment strategy and reducing fees, you can potentially achieve higher returns. For example, aiming for 12-14% annual returns could shorten your path to financial freedom significantly, from 40 years to perhaps 25 years. This improvement comes from smarter investing, not necessarily investing more money or changing your lifestyle.

Key takeaways for investors:

- Review Expense Ratios: Understand and minimize the fees in your 401(k).

- Consider Tax Implications: Decide if a Traditional or Roth 401(k) best suits your financial situation.

- Calculate Your Needs: Do the math to determine how much you truly need to retire comfortably and assess if your current 401(k) is on track.

- Seek Better Returns: Explore ways to optimize your investments for potentially higher growth, whether within your 401(k) or through other investment vehicles.

A 401(k) is a starting point, but it was never meant to be your only retirement plan. Taking control of your financial education and making informed investment decisions are crucial for achieving wealth and financial freedom sooner.

Source: Watch This Before Putting Money in Your 401(k) — The Truth Nobody Knows (YouTube)