47% of Americans Struggle with $1,000 Emergency Expenses, Highlighting Systemic Financial Issues Beyond Income

A striking statistic reveals that 47% of Americans report being unable to cover a $1,000 emergency expense, a reality that transcends income brackets, affecting even those earning six figures. This data underscores a critical insight: financial well-being is not solely dictated by income but by the presence of a robust financial system and adequate awareness. Individuals who lack a coherent strategy for managing their earnings often find themselves perpetually feeling financially strained, regardless of their salary.

The Awareness Gap: The ‘Ostrich Effect’ in Personal Finance

The chasm between financial struggle and wealth creation often lies not in income disparity but in a fundamental lack of awareness regarding one’s financial standing. This is particularly evident in tracking expenses. A recent informal poll of 80 college students found that only one individual actively tracked their spending. This avoidance of financial reality is so prevalent that behavioral economists have termed it the ‘ostrich effect’ – the tendency to ignore negative financial information rather than confront it.

Research cited indicates that individuals who do not regularly monitor their accounts exhibit more erratic spending patterns, especially around payday. Furthermore, infrequent account checkers tend to spend significantly more on discretionary items compared to their diligent counterparts. The solution, while simple, requires a shift in habit: regular financial monitoring. Utilizing budgeting apps, spreadsheets, or even a simple notebook can provide the necessary baseline awareness.

Subscription Overload: The Hidden Cost of Convenience

Another significant drain on personal finances is the proliferation of subscriptions. While individuals estimate spending around $86 per month on subscriptions, the actual average is over $219 per month. Nearly one in three people underestimate their subscription spending by a staggering $100 to $199 monthly. The ease with which services are subscribed to, often with a single click, contrasts sharply with the convoluted cancellation processes, creating a financial trap.

A crucial step is conducting a thorough subscription audit. Listing all recurring services and evaluating their active usage and value proposition is essential. If a subscription cannot be definitively justified as worthwhile, it represents a prime candidate for cancellation.

Emotional and Social Spending: The Psychological Pitfalls

Beyond awareness, spending habits are often driven by emotional and social factors. While about 5% of the population may experience compulsive buying disorder, a larger segment engages in emotional spending – using purchases to cope with sadness, loneliness, or stress. Even seemingly minor indulgences, like a $7 ice cream treat to lift spirits, can accumulate significantly over time.

Developing emotional intelligence, which involves better regulation and recognition of one’s emotions, is negatively correlated with impulsive buying. This suggests that managing emotional triggers is a skill that can be learned and improved.

Social spending presents another challenge, with peer pressure compelling individuals to participate in activities that may strain their budgets. The average individual spends $250 per month on social activities, amounting to over $3,000 annually. This pressure can lead to overspending to keep up or missing out due to financial constraints, a lose-lose scenario without a plan.

To combat emotional and social spending, a three-point checklist can be invaluable: 1) Do you genuinely need this item? 2) Does it move you closer to your financial goals? 3) Does it align with your values? Answering ‘no’ to any of these questions should prompt a pause and reconsideration of the purchase. Honesty with friends about financial limitations is also key to navigating social pressures authentically.

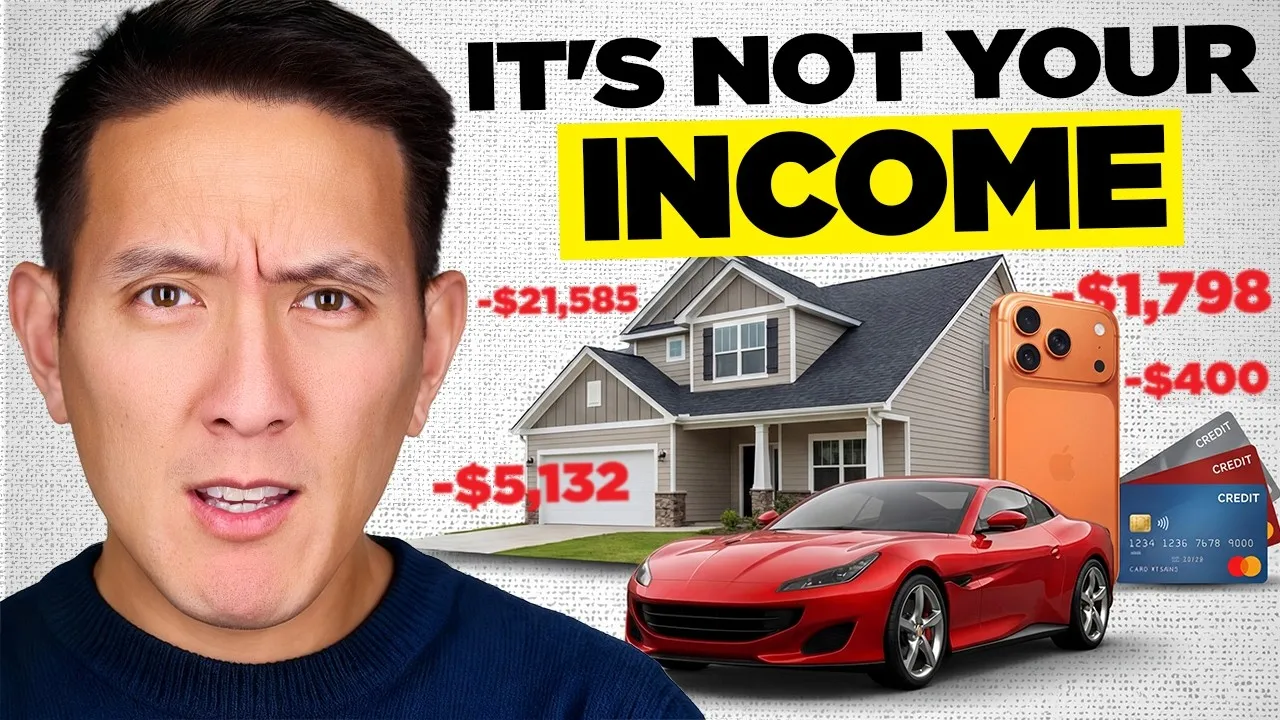

The Big Purchase Trap: Overextending on Cars and Housing

While managing small, recurring expenses is vital, the most significant financial pitfalls often arise from large, recurring purchases. The temptation to justify a large expenditure after being diligent with smaller ones can lead to locking into expensive car or housing payments. These two categories typically account for 50-60% of a person’s monthly expenses, making miscalculations here particularly detrimental.

The average new car payment hovers around $750 per month, with nearly 19% of car owners paying over $1,000 monthly. The trend towards longer loan terms, now averaging over 68 months, exacerbates this issue. A common mistake is immediately taking out a new car loan after paying off a previous one, rather than maximizing the lifespan of existing vehicles.

Housing costs present a similar challenge. With median home prices around $410,000-$450,000, many individuals overextend themselves to meet the perceived ideal of homeownership. Banks may qualify borrowers for loans exceeding their actual affordable capacity, leading to financial strain.

To mitigate these risks, affordability rules are crucial. For vehicles, the 20-4-10 rule suggests a 20% down payment, a loan term of no more than 4 years, and total transportation costs (including insurance and fuel) not exceeding 10% of gross monthly income. For housing, the 28% rule advises that monthly mortgage payments, including principal, interest, taxes, and insurance (PITI), should not exceed 28% of gross monthly income. For example, a $400,000 home, with a 20% down payment and including PITI, might require a salary of around $112,000 to be affordable under this rule, illustrating the gap between bank qualification and true affordability.

The Power of a Financial Plan: Saving First, Spending Later

A staggering 92% of people fail to achieve their financial goals, often due to a lack of an actionable plan rather than ambition. Many treat saving as an afterthought, spending what remains after bills and discretionary purchases. This backward approach typically leaves little to no money for savings, often leading to debt.

The effective solution is to reverse this process: save first, then spend what remains. Automating savings, as supported by Consumer Financial Protection Bureau studies showing participants saving twice as much ($167 vs. $80 per month) when enrolled in automatic plans, is highly effective. This ‘pay yourself first’ method ensures savings occur before discretionary spending, making it a natural part of the financial flow.

Leveraging ‘Free Money’: The 401(k) Match and Tax Advantages

Perhaps the most straightforward, yet often overlooked, strategy is to capitalize on ‘free money.’ Employer-sponsored 401(k) plans frequently offer matching contributions, effectively doubling immediate contributions up to a certain percentage. Despite this guaranteed 100% return, approximately one in four workers do not contribute enough to receive the full employer match, leaving an average of $1,360 per year on the table. Over 40 years, this foregone amount, compounded, can exceed $45,000.

For those without employer-sponsored plans or in different tax jurisdictions, exploring tax-advantaged retirement accounts, such as a Roth IRA in the U.S., is crucial. Roth IRAs allow earnings to grow and be withdrawn tax-free in retirement, offering a significant return on investment by eliminating future tax liabilities on gains.

Market Impact and Investor Takeaways

The financial habits discussed—lack of tracking, excessive subscriptions, emotional spending, overextending on major purchases, poor planning, and neglecting ‘free money’ opportunities—collectively illustrate a widespread disconnect between earning potential and wealth accumulation. These behavioral patterns directly impact consumer spending, savings rates, and debt levels, influencing broader economic trends and market sentiment. For investors, understanding these common financial missteps is key to recognizing that building wealth is often more about disciplined execution of fundamental financial principles than about chasing complex investment strategies.

What Investors Should Know:

- Behavioral Finance is Key: Recognizing and addressing personal financial behaviors like the ‘ostrich effect’ or emotional spending is foundational to financial health and, by extension, investment capacity.

- Debt Management is Paramount: High-interest debt, often a consequence of poor spending habits and overextended major purchases, erodes an investor’s ability to save and invest.

- The Power of Compounding: Even small, consistent savings and investments, particularly those boosted by employer matches or tax advantages, can grow significantly over time due to compounding.

- Affordability Over Qualification: Relying on bank-qualified loan amounts for major purchases like homes and cars often leads to overextension. Adhering to personal affordability rules is critical for long-term financial stability.

- Systematic Planning Pays Off: Implementing a clear financial plan, prioritizing saving through automation, and taking advantage of all available financial benefits (like 401(k) matches) are direct pathways to improved financial outcomes.

Source: You're Not Poor, You're Just Bad With Money (YouTube)