30-Year Mortgages Double Interest Costs: A Hidden Debt Trap

A prevailing financial habit, particularly in the housing market, is the seemingly attractive option of a 30-year mortgage over its 15-year counterpart. While the lower monthly payment of a 30-year loan offers immediate relief, emerging analysis suggests this choice can lead to significantly higher long-term costs, potentially doubling the interest paid and encouraging over-borrowing.

The Allure of Lower Monthly Payments

For many homebuyers, the primary driver behind selecting a 30-year mortgage is the immediate affordability. The extended repayment period allows for smaller, more manageable monthly installments compared to the more aggressive payment schedule of a 15-year loan. This difference can free up immediate cash flow, which borrowers often rationalize as a way to invest elsewhere or simply to make homeownership more accessible.

The psychological appeal is strong: a lower payment feels safer, and the promise of paying off the loan eventually, perhaps even faster than the stated term, provides comfort. However, research and historical data indicate that this intention is rarely realized.

The Unseen Cost of Extended Terms

The core issue lies in the structure of mortgage amortization. In a 30-year loan, a larger portion of the early payments is allocated to interest rather than principal.

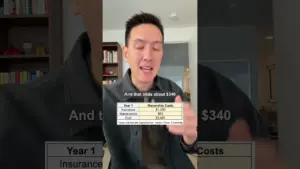

This means that over the life of the loan, a significantly greater amount of money is paid to the lender in interest charges. Specifically, opting for a 30-year mortgage can result in paying more than double the total interest compared to a 15-year loan on the same principal amount.

“The 30-year sort of hides the fact that you were carrying a whole lot of debt on top of paying a whole lot of interest in the 30-year versus 15 over double.”

This disparity in interest costs represents a substantial financial burden that accumulates over time. While the immediate monthly savings might seem beneficial, the long-term financial impact can be profound, affecting a borrower’s net worth and financial flexibility for decades.

Behavioral Economics and Housing Decisions

The decision-making process around mortgage selection is often influenced by behavioral biases. The immediate gratification of a lower monthly payment outweighs the deferred cost of higher interest.

This is compounded by a general tendency for individuals to underestimate future financial discipline. The assumption that one will actively seek to pay down the principal faster on a 30-year loan is, according to available research, largely unfounded.

The extended repayment period of a 30-year mortgage can inadvertently encourage borrowers to purchase more expensive homes than they might otherwise afford. The lower monthly payment masks the true cost of carrying that larger debt, leading to a situation where individuals might overextend themselves financially. A 15-year mortgage, by contrast, imposes a stricter discipline, forcing a more realistic assessment of affordability and discouraging the purchase of homes that stretch financial resources too thin.

Market Impact and Investor Considerations

The prevalence of 30-year mortgages has significant implications for the broader housing market and the financial sector. Lenders benefit from the sustained interest income over a longer period. For investors in mortgage-backed securities, the extended duration of these loans provides a predictable, long-term income stream.

However, for individual homeowners, the choice has direct consequences on their wealth accumulation. The additional funds spent on interest could otherwise be invested in higher-return assets, contribute to retirement savings, or be used for other financial goals. This opportunity cost is a critical factor that many borrowers overlook when making their initial mortgage decision.

What Investors Should Know

The enduring popularity of the 30-year mortgage highlights a persistent disconnect between immediate financial comfort and long-term wealth building. While the lower monthly payment offers a psychological buffer, the financial penalty in terms of doubled interest payments is a significant factor for homeowners to consider.

- Interest Cost Differential: A 30-year mortgage typically results in paying more than twice the amount of interest compared to a 15-year mortgage on the same principal.

- Affordability Illusion: Lower monthly payments can mask the true cost of debt and may encourage overspending on housing.

- Behavioral Tendencies: The intention to pay off a 30-year mortgage early is often not realized, leading to higher long-term expenses.

- Opportunity Cost: Funds spent on excess interest could be allocated to investments or other financial goals, impacting long-term wealth accumulation.

For prospective homebuyers, a thorough analysis of total interest paid over the life of the loan, rather than solely focusing on the monthly payment, is crucial. Understanding the long-term financial implications can lead to more prudent borrowing decisions and better financial outcomes. While the 30-year mortgage serves a purpose in making housing accessible, its hidden costs warrant careful consideration by anyone entering the property market.

Source: This is an Unpopular Opinion for Sure (YouTube)