Stocks Navigate Uncertainty Amid Geopolitical Tensions and Financial Sector Scrutiny

U.S. Stock markets exhibited a mixed performance as investors grappled with a complex interplay of geopolitical developments, central bank policy expectations, and emerging concerns within the private credit sector. While some technology stocks showed resilience, broader market sentiment was tempered by ongoing tensions in the Middle East and a notable incident mirroring the liquidity crunches of 2007.

OpenAI’s $100 Billion Funding Round Boosts Tech Sentiment

A significant development providing a tailwind for the technology sector was OpenAI’s announcement of securing commitments for a $100 billion funding round. Major players like Amazon, reportedly considering a $50 billion contribution, and Nvidia, pledging $30 billion, alongside SoftBank’s $30 billion installment plan, signaled strong investor confidence in the artificial intelligence leader.

While much of this anticipated funding was already factored into market expectations, the finalized commitments offer a tangible boost, enabling continued investment in research, development, and chip procurement. Analysts are closely watching the second-order effects of this funding on sales for companies like Nvidia and Super Micro Computer.

Tech Sector Innovations and Competition

Beyond funding, innovation continues to drive competition. Meta is reportedly reviving plans for a smartwatch, potentially entering a market dominated by Apple. This move follows Meta’s success with its augmented reality glasses, a product category that has also piqued Apple’s interest, suggesting a growing battleground in wearable and immersive technologies.

Geopolitical Flashpoints: Middle East Tensions Escalate

The Middle East remains a focal point of geopolitical concern, with reports indicating the largest concentration of air power in the region since the 2003 invasion of Iraq. Op-eds suggest that the Trump administration holds significant leverage over Iran, with various potential outcomes ranging from regime change to a negotiated deal.

The uncertainty surrounding potential U.S. Military action, coupled with Iran’s nuclear ambitions, introduces a layer of risk for oil markets and global stability. President Trump has indicated a decision on potential strikes would be made within the next 10 days, a timeframe that markets are closely monitoring.

Private Credit Sector Echoes 2007 Liquidity Fears

A more concerning development emerged from the private credit sector, drawing parallels to the liquidity crisis of 2007. Blue Owl Capital announced it would restrict withdrawals from one of its retail-focused private credit funds. This move, which shifts redemptions from quarterly to periodic distributions funded by loan repayments or asset sales, echoes the actions of BNP Paribas in August 2007, when it froze $2.2 billion in funds due to issues in the subprime mortgage sector.

The inability to calculate asset values and redeem cash, a hallmark of the 2007 crisis, is now raising similar concerns in the less transparent private credit market. Blue Owl’s situation is further complicated by a failed merger attempt and ongoing efforts to wind down legacy vehicles.

This incident highlights the inherent risks in the rapidly expanding private credit sector, particularly for retail investors. The lack of liquidity in certain market segments, as experienced by Blue Owl, suggests that the broader market may be underestimating the systemic risks accumulating in private credit. The valuation of publicly traded vehicles for private equity, like Blue Owl’s tech fund trading at a 30% discount to its book value, offers a rare glimpse into potential distress, while the opacity of non-public private equity firms could be masking larger issues.

Corporate Earnings and Sector Specifics

In corporate news, DoorDash reported strong growth in deliveries, with its stock showing a rebound near the $163 level, eyeing a test of the $192 resistance. Conversely, Carvana experienced a significant sell-off, down approximately 6% in regular trading and as much as 22% in after-hours trading. The company’s business model, perceived by some as a circular financing operation where insiders sell stock to finance receivables, faces ongoing scrutiny.

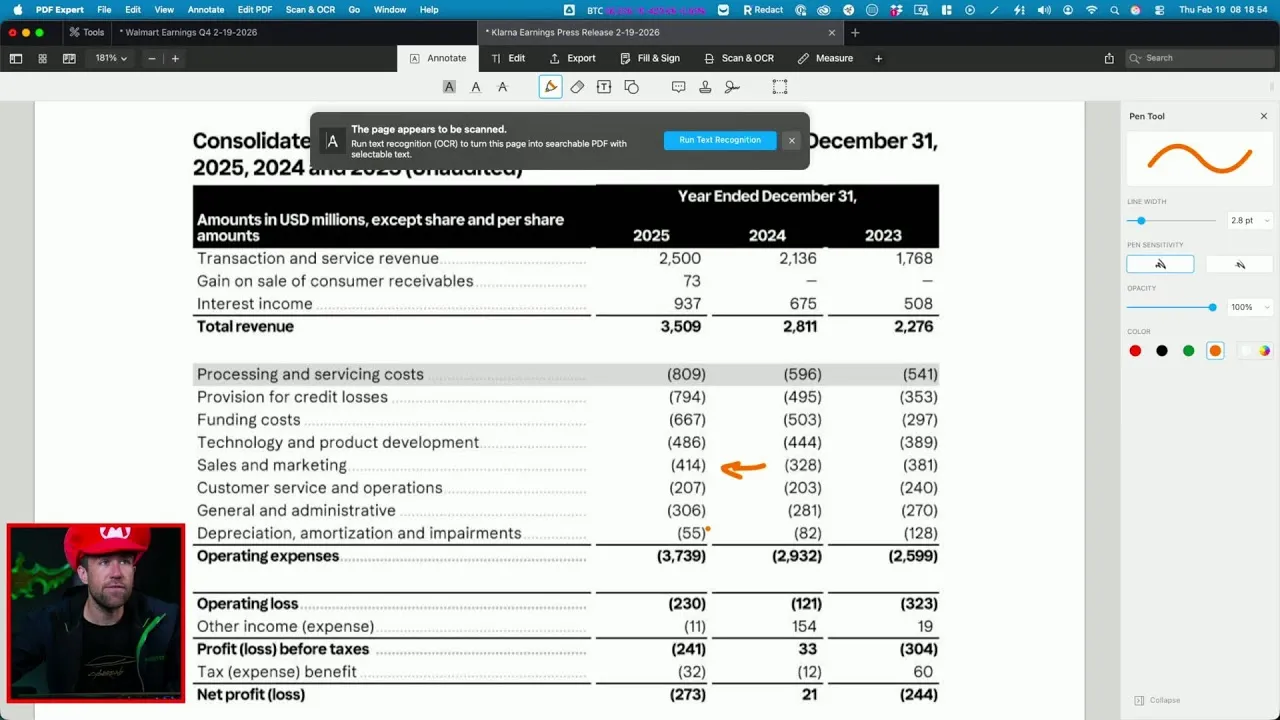

Walmart issued a cautious outlook, missing its own projections and taking a $2.1 billion loss on a Symbiotic position. The retail giant also faces scrutiny over its debt levels, with analysts pointing to a significant shortfall in liquid assets to cover short-term liabilities, potentially necessitating further borrowing despite current dividend payouts and stock buybacks.

In the tech space, Microsoft’s stock dipping below the $400 level was noted as a bearish signal for short-term traders, acting as a ‘canary in the coal mine’ alongside AMD’s retreat from its $200 level. A sustained decline below these technical benchmarks could signal further downside for the broader market.

Market Impact

What Investors Should Know:

- Geopolitical Risk Premium: Escalating tensions in the Middle East could lead to increased volatility, particularly in energy markets.

- Private Credit Scrutiny: The Blue Owl situation is a cautionary tale regarding liquidity risks and valuation transparency in private credit. Investors should exercise caution with funds exhibiting redemption restrictions.

- Federal Reserve Policy Uncertainty: Market optimism regarding potential Federal Reserve rate cuts may be misplaced if economic data remains robust, creating a double-edged sword for equities.

- Technical Levels to Watch: Key support levels for the Nasdaq 100 (Q’s) and individual stocks like Microsoft and AMD are critical indicators of short-term market direction.

Long-Term Outlook

The current market environment presents a challenging outlook for the next six months. A scenario where the Federal Reserve refrains from cutting interest rates due to strong job growth could remove a key tailwind for stocks. Conversely, a significant slowdown in job creation would also be detrimental, signaling economic weakness.

This creates a complex environment where rate cuts might not materialize as expected, potentially capping market upside. Investors are advised to monitor economic data closely and remain adaptable to shifting policy expectations.

Source: Stocks Mixed on Fed, Iran, and Rates (YouTube)