Consumers Routinely Underestimate Monthly Expenses

New insights from behavioral economics suggest a significant disconnect between what individuals believe they spend and their actual outlays. Studies indicate that most people underestimate their monthly spending by a substantial margin, ranging from 25% to as high as 40%. This considerable blind spot can impede financial progress and hinder effective budgeting.

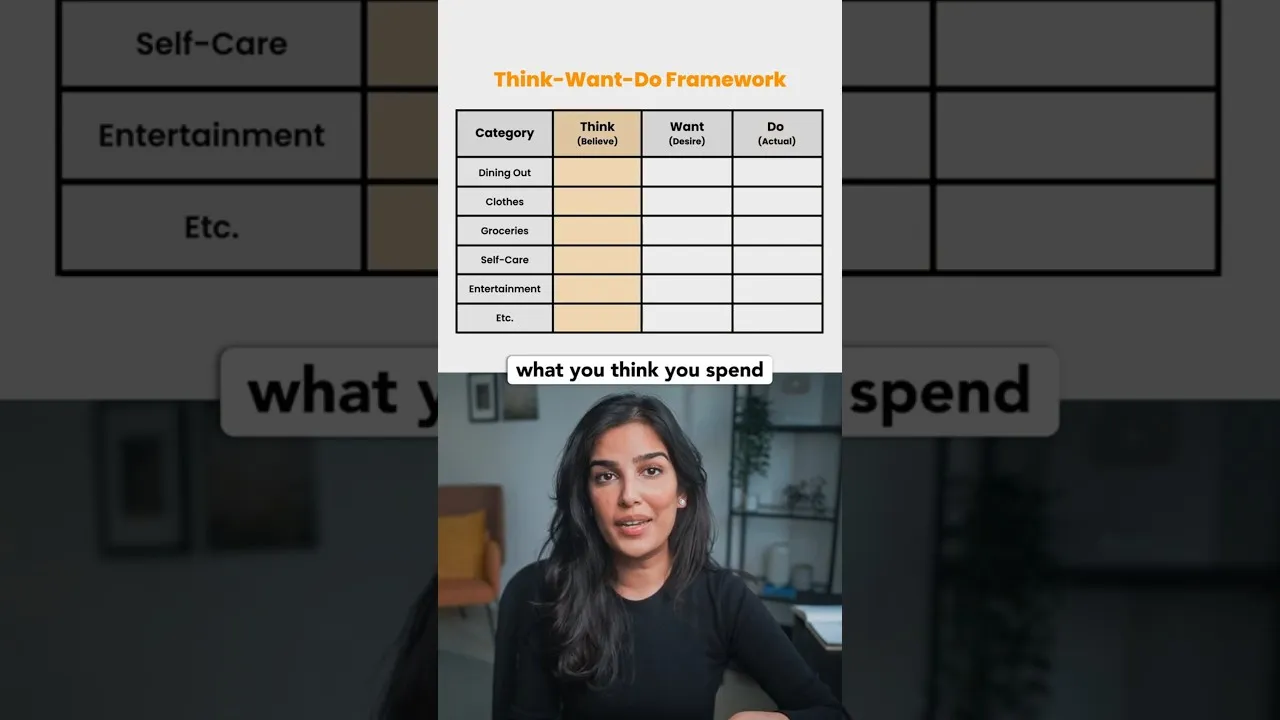

The ‘Think-Want-Do’ Framework

To address this common financial oversight, a framework known as ‘Think-Want-Do’ has been proposed to help individuals bridge the gap between perceived and actual spending. This methodology breaks down money habits into three distinct phases:

- Think: The initial step involves listing your estimated monthly expenses by category. This reflects your current perception of where your money goes.

- Want: Next, you define your desired spending levels for each category. This sets a target or ideal budget.

- Do: The final and most crucial phase is to track what you actually spend. This ‘Do’ section provides a reality-based starting point for your financial assessment.

Bridging the Perception Gap

Regularly comparing your ‘Think’ (estimated spending) with your ‘Do’ (actual spending) is essential. This comparison highlights discrepancies and brings awareness to spending habits that may have gone unnoticed. Behavioral economists suggest that this process helps to fine-tune financial instincts, creating a natural feedback loop.

As individuals become more attuned to their spending patterns through this iterative process, they are better positioned to make more informed and effective financial decisions. This heightened awareness can lead to more realistic budgeting, improved savings, and ultimately, greater financial stability.

Market Impact and Investor Considerations

While this framework directly addresses personal finance, the underlying principle of consumer spending underestimation has broader economic implications. Consumer spending is a primary driver of economic growth, accounting for a significant portion of Gross Domestic Product (GDP) in most developed economies. A consistent overestimation of savings capacity or underestimation of expenditure could lead to:

- Reduced Disposable Income: If consumers are consistently spending more than they realize, their actual disposable income for savings or discretionary purchases may be lower than anticipated.

- Impact on Retail and Consumer Goods Sectors: Misjudged consumer spending can affect demand forecasts for businesses in the retail, consumer discretionary, and even consumer staples sectors. Companies relying on accurate consumer behavior predictions might face challenges.

- Interest Rate Sensitivity: If households consistently underestimate their debt servicing costs or overcommit based on perceived available funds, they may become more vulnerable to interest rate hikes, potentially impacting credit markets and the broader economy.

- Inflationary Pressures: A widespread underestimation of spending could, in aggregate, contribute to higher demand than anticipated, potentially exacerbating inflationary pressures if supply cannot keep pace.

What Investors Should Know

For investors, understanding consumer behavior is paramount. The ‘Think-Want-Do’ discrepancy highlights a potential disconnect between stated consumer confidence or intentions and actual financial realities. Investors should consider:

- Data Granularity: Relying on aggregate consumer spending data might mask underlying trends. Understanding how different income brackets or demographics perceive and execute their spending is crucial.

- Company Guidance: When analyzing companies, particularly those in consumer-facing sectors, scrutinize their assumptions about consumer spending habits. Are they based on realistic assessments or potentially flawed perceptions?

- Economic Indicators: While headline consumer spending figures are important, investors should look for indicators that reflect actual spending velocity and debt levels, such as credit card debt trends, personal savings rates, and retail sales data adjusted for inflation.

- Long-Term Trends: The behavioral aspect suggests that financial literacy and awareness programs could, over the long term, lead to more stable and predictable consumer spending patterns. This could benefit sectors that rely on consistent consumer demand.

The persistent tendency for individuals to underestimate their spending highlights the importance of diligent financial tracking and realistic budgeting. This behavioral insight, while personal, carries implications for economic forecasting and investment strategies that depend on accurate assessments of consumer activity.

Source: Do you underestimate your spending? #moneytips (YouTube)