Emergency Funds: You Need Less Than You Think

Many individuals overestimate the size of their emergency fund, leading to significant sums of cash sitting idle and losing value. Financial experts suggest a more precise approach based on essential living expenses, potentially freeing up capital for investment.

The Pitfalls of Over-Saving

During a career in banking, it became apparent that many professionals held substantial amounts in their savings accounts, believing it was designated for emergencies. Balances ranging from $40,000 to $70,000 were not uncommon.

However, a closer examination of their actual monthly expenditures revealed a different picture. When stripping away non-essential spending and focusing solely on core living costs—such as mortgage or rent payments, groceries, essential utilities, and minimum debt obligations—the true emergency fund requirement was often less than half of these substantial holdings.

The remainder, often termed “fear money,” sat in accounts, subject to inflation and failing to generate any meaningful returns. This highlights a common misconception: the purpose of an emergency fund is to cover essential living costs during a complete loss of income, not to serve as a buffer for every conceivable financial contingency or a repository for excess cash.

Calculating Your True Emergency Fund Needs

The fundamental principle of an emergency fund is to ensure financial stability during periods of unexpected income disruption. The recommended calculation is straightforward and personalized:

- Identify Core Living Expenses: Tally up all your essential monthly costs. This includes housing (rent or mortgage), utilities, groceries, transportation to work, insurance premiums, and minimum payments on debts.

- Determine Your Multiplier:

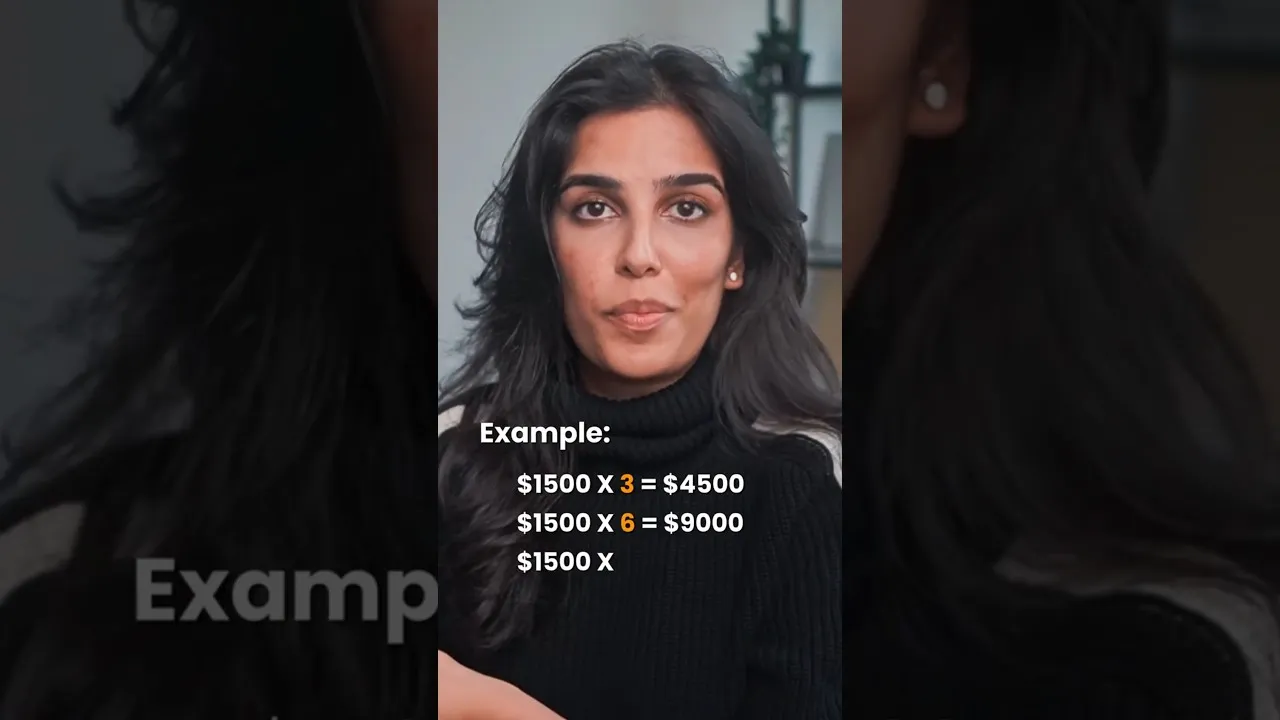

- Basic Fund: Multiply your total core monthly living expenses by three. This provides a foundational safety net.

- Enhanced Protection: For greater peace of mind, multiply your core monthly expenses by six. This offers a more robust cushion against prolonged unemployment.

- High-Risk Employment: If you are self-employed or work in an industry with high job instability, consider multiplying your core monthly expenses by nine. This accounts for a potentially longer period without income.

For instance, if your essential monthly living expenses total $3,000, a basic emergency fund would require $9,000 ($3,000 x 3). An enhanced fund would be $18,000 ($3,000 x 6), and for those in high-risk employment, it could be as much as $27,000 ($3,000 x 9).

Market Impact and Investor Considerations

The implication of this refined approach to emergency funds is significant for individual investors. Holding excessive cash in low-yield savings accounts can lead to a substantial opportunity cost. Inflation erodes the purchasing power of this idle money, while investment markets, over the long term, have historically offered higher returns.

What Investors Should Know

- Opportunity Cost: Cash held as an excessively large emergency fund is not working for you. These funds could be invested in assets like stocks, bonds, or real estate, which have the potential to grow over time and outpace inflation.

- Inflationary Erosion: In an environment of rising prices, cash savings lose value. The $50,000 in an account earning 0.5% interest while inflation is at 3% is effectively losing 2.5% of its purchasing power annually.

- Risk Management vs. Fear: Differentiating between prudent risk management and emotional “fear money” is crucial. An emergency fund is a tool for managing specific risks (job loss, unexpected major expenses), not a blanket solution for all financial anxieties.

- Diversification of Savings: Once the appropriate emergency fund is established and held in a liquid, safe account (like a high-yield savings account), surplus funds can be strategically allocated to a diversified investment portfolio aligned with long-term financial goals.

The principle extends beyond individual savings to broader market sentiment. When individuals hoard cash due to perceived economic uncertainty, it can dampen consumer spending and investment, potentially slowing economic growth. Conversely, a more confident approach, backed by an adequately sized, but not excessive, emergency fund, can encourage greater participation in the economy and capital markets.

Long-Term Implications

For the average individual, understanding and implementing this precise emergency fund calculation can unlock capital that can be invested for long-term wealth creation. While the exact figures vary based on individual circumstances, the core principle remains: calculate your needs, secure them, and then let the rest work towards your future financial security through informed investment strategies. This approach not only protects against immediate financial shocks but also contributes to building wealth over the long haul, a critical component of comprehensive financial planning.

Source: How much do you need to save for emergencies? #moneytips (YouTube)