Inflation’s Silent Tax: Why Cash is a Losing Proposition

In an environment where inflation continues to chip away at purchasing power, holding excess cash in bank accounts is proving to be a financially detrimental strategy. While seemingly safe, idle cash is effectively losing value year over year, acting as the “laziest worker” in an investor’s portfolio. This passive approach, born from hard-earned income, fails to generate any returns and is actively diminished by rising prices.

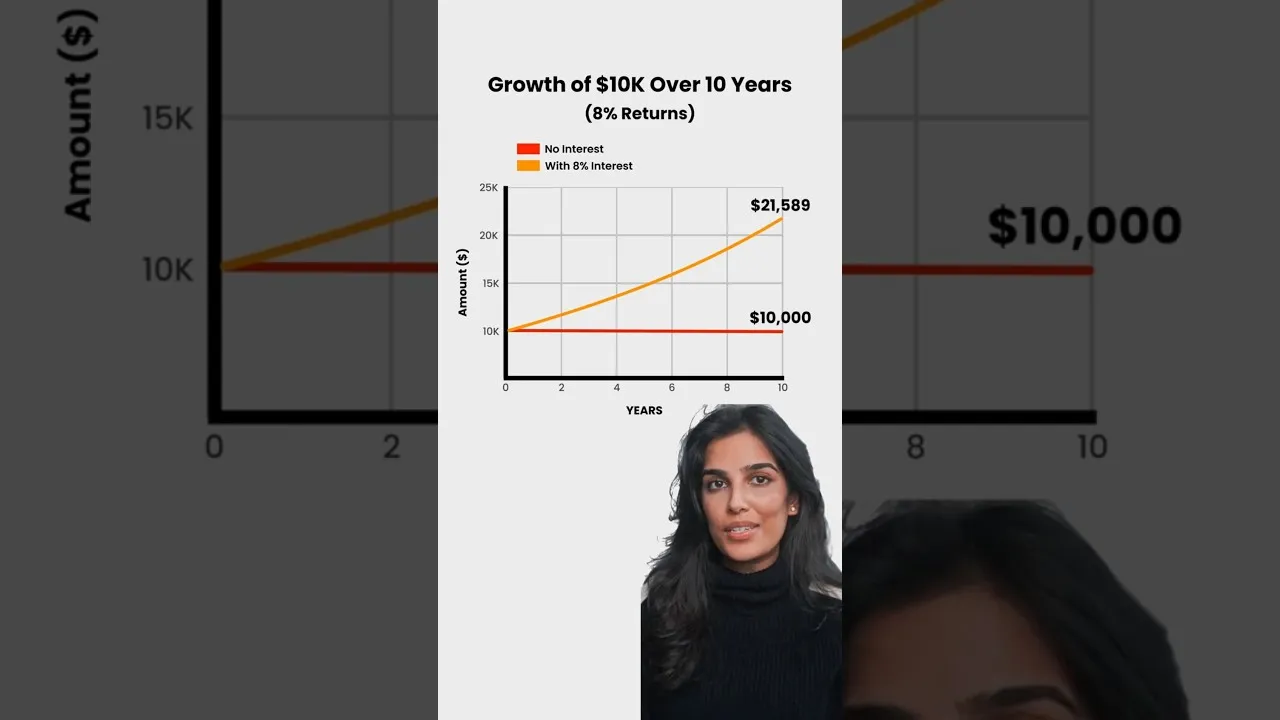

The Power of Compounding: Turning $10,000 into Over $21,000

Consider a scenario where an individual saves $10,000. If this sum remains in a standard bank account, it will still be $10,000 after a year. However, due to inflation, its real value – what it can actually purchase – will have decreased.

In contrast, if that same $10,000 is invested in an asset that yields an average annual return of 8% over a decade, the outcome is dramatically different. After 10 years, that initial $10,000 could grow to over $21,000. This represents more than a doubling of the original capital, generating an additional $11,000 purely through the power of investment growth, without requiring any further sacrifice of time or labor.

Understanding Inflation and Its Impact on Savings

Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. When the inflation rate exceeds the interest rate earned on cash deposits, savers experience a negative real return.

For instance, if inflation is running at 5% and a savings account yields 1%, the real return is -4%. This means that while the nominal amount of money in the account increases slightly, its ability to buy goods and services diminishes significantly over time.

What Investors Should Know

- The Cost of Inaction: Letting money sit in cash is not a risk-free strategy. The primary risk is the erosion of purchasing power due to inflation.

- The Potential of Growth: Investing, even with modest returns, can significantly outperform cash over the long term. The example illustrates how an 8% annual return can more than double an initial investment in 10 years.

- Compounding is Key: The growth of investments is often driven by compounding, where earnings from an investment are reinvested, generating their own earnings. This snowball effect accelerates wealth accumulation over time.

Sector and Asset Class Considerations

While the transcript highlights a general investment principle, the specific assets that can achieve an 8% annual return vary. Historically, broad market equity indices like the S&P 500 have delivered average annual returns in this range over long periods, though past performance is not indicative of future results. Other asset classes, such as bonds or real estate, may offer different risk-return profiles.

The choice of investment should align with an individual’s risk tolerance, time horizon, and financial goals. Diversification across different asset classes is often recommended to manage risk.

Long-Term Implications for Investors

For long-term investors, the implications are clear: a strategy centered around accumulating wealth must involve putting capital to work. Relying on cash savings to preserve or grow wealth in the face of inflation is a flawed approach.

The power of compound growth, demonstrated by the hypothetical doubling of savings over a decade, highlights the importance of starting early and staying invested. Even small amounts invested consistently can grow substantially over time, helping individuals achieve their financial objectives, whether it’s retirement, a down payment on a house, or other significant life goals.

“Cash is the laziest worker you’ll hire. You worked overtime. You sacrificed your evenings to make, say, 10,000. And you put it in a bank account. You check that bank account after a year. And your money has just sat there, been lazy, and hasn’t created any more money for you. Not only that, but it’s now also worth less than it was a year ago because of inflation.”

The core message is to shift from a mindset of passive cash holding to active wealth creation. By understanding the detrimental effects of inflation on stagnant capital and harnessing the potential of investment returns, individuals can significantly enhance their financial future.

Source: Don’t keep your money in cash. Here’s what to do instead #savingmoney #moneytips (YouTube)