Government Introduces ‘Trump Accounts’ Offering Up to $1,000 Per Child

A new government initiative, dubbed ‘Trump Accounts,’ aims to provide financial incentives for families with newborns and young children. The program offers an initial deposit of $1,000 for children born between January 1, 2025, and December 31, 2028, and a $250 bonus for eligible children under the age of 10. These accounts are structured as tax-advantaged, IRA-style vehicles designed for individuals under 18.

Program Details and Eligibility

To qualify for the $1,000 initial deposit, a child must be born within the specified 2025-2028 timeframe and possess a Social Security number. The funds are automatically invested in low-cost U.S. Stock index funds.

The $250 bonus is designated for children aged 10 and under, born prior to 2025. Eligibility for this bonus is tied to the child’s zip code, specifically requiring a median household income below $150,000 in that area, rather than the family’s personal income.

Contribution Limits and Long-Term Growth Potential

Beyond the initial government contributions, family members, friends, and employers can contribute up to $5,000 annually to a Trump Account until the child reaches the age of 18. At this juncture, the account transitions into a traditional Individual Retirement Arrangement (IRA).

The potential for long-term growth is significant. If an account is opened at birth and consistently maxed out with the $5,000 annual contribution until age 18, the total personal contributions would amount to $90,000.

While the projected value at age 18 is approximately $22,000 (implying a substantial portion is government contribution and early growth), the long-term outlook is more dramatic. If left untouched until age 65, such an account could potentially grow to an estimated $7.52 million.

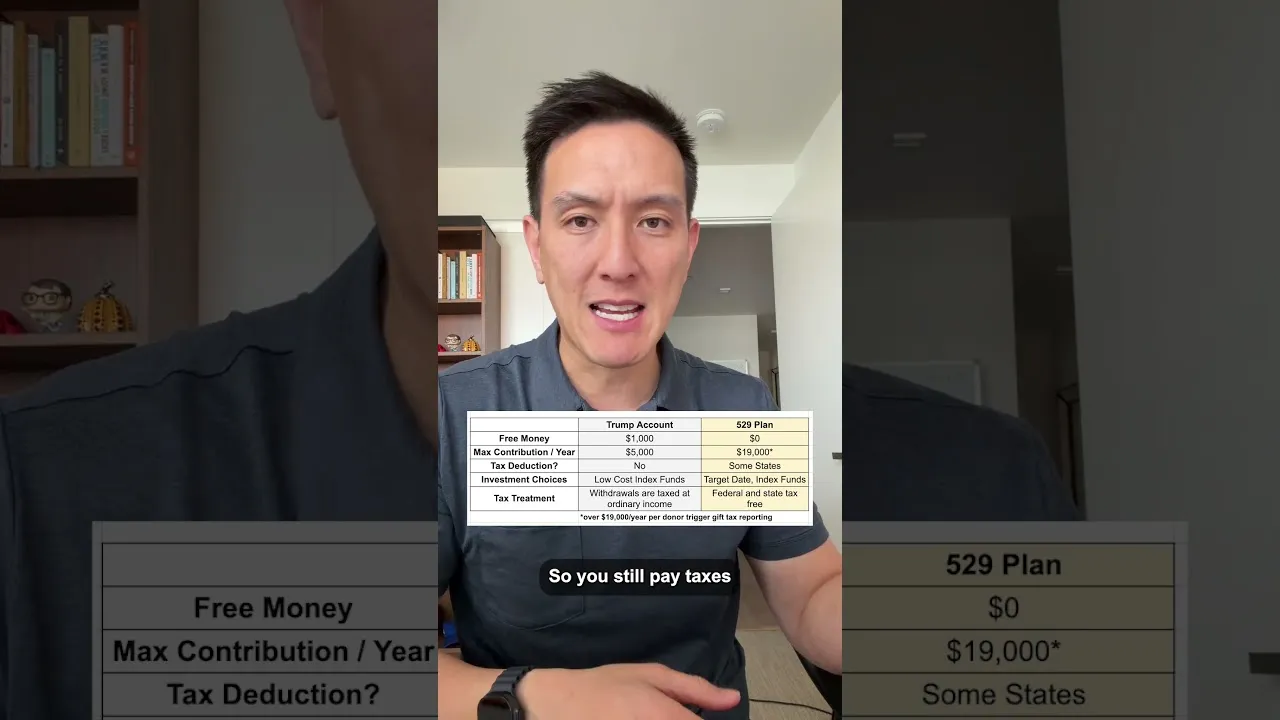

Comparison with 529 Plans

While Trump Accounts offer an initial government incentive, comparisons are being drawn with existing savings vehicles like 529 plans, primarily used for education expenses. The primary distinction lies in taxation. 529 plans offer tax-free growth and tax-free withdrawals when used for qualified education expenses. In contrast, Trump Accounts, upon converting to a traditional IRA, will be subject to taxes on earnings during withdrawal, similar to a traditional IRA.

The stated uses for Trump Account funds include education, a first-time home purchase, or starting a business. However, clarity is still pending on the specific withdrawal mechanisms and tax implications once the account converts to a traditional IRA.

Opening an Account and Key Dates

The application process for a Trump Account is straightforward. Interested parties can visit form.trumpaccounts.gov to complete an online form.

Alternatively, individuals can submit Form 4547 with their 2025 tax return, providing the child’s information. Multiple copies of the form can be submitted for families with more than two children.

A key date to note is July 5, 2026. This is the date when the initial $1,000 deposits are expected to be disbursed, and contributions to the accounts can commence.

Account Management and Future Updates

Initially, Trump Accounts will be held by financial institutions designated by the Treasury. Provisions for transferring these accounts to brokerage accounts at a later stage are anticipated, though the specific institutions and brokerages involved remain to be announced.

For ongoing updates and further details as they become available, interested individuals are encouraged to follow relevant announcements.

Market Impact and Investor Considerations

The introduction of Trump Accounts represents a novel government-led initiative to encourage long-term savings for children. While the direct market impact is likely to be modest initially, the program could influence savings behaviors and potentially direct capital towards U.S. Equity markets through the mandated index fund investments.

What Investors Should Know:

- Government Seed Capital: The $1,000 and $250 bonuses provide an immediate, risk-free starting point for savings, particularly for newborns.

- Tax Implications: Understand the difference between the Trump Account’s eventual IRA status (taxable withdrawals on earnings) and the tax-free nature of 529 plans for qualified education expenses.

- Long-Term Growth: The potential for significant wealth accumulation by age 65, driven by compounding returns, is a key feature, assuming consistent contributions.

- Contribution Flexibility: The ability for family, friends, and employers to contribute offers a structured way to support a child’s financial future.

- Uncertainty on Withdrawals: Clarity is needed regarding the specific rules and tax treatments for withdrawals after the account converts to a traditional IRA, especially for non-retirement purposes.

From a financial planning perspective, the Trump Account could serve as a valuable supplement to existing savings strategies. Given the lack of apparent downside to accepting the initial government contribution and allowing it to grow, it presents an opportunity for families to begin saving early. However, a comprehensive review of financial goals, including education funding and retirement planning, should guide decisions on whether to maximize contributions beyond the initial government deposit, especially when compared to other tax-advantaged vehicles like 529 plans.

Source: The government wants to give you $1,000 free for your kid (YouTube)