Howard Marks’ ‘The Most Important Thing’ Offers Timeless Investment Wisdom

Legendary investor and billionaire Howard Marks, in his seminal work ‘The Most Important Thing,’ provides a framework for navigating the complexities of the financial markets. Summarized from a recent analysis, Marks’ core tenets emphasize strategic positioning, profound analytical thinking, and a disciplined approach to risk management. These principles offer investors a robust guide to achieving superior returns, moving beyond mere speculation to cultivate genuine insight.

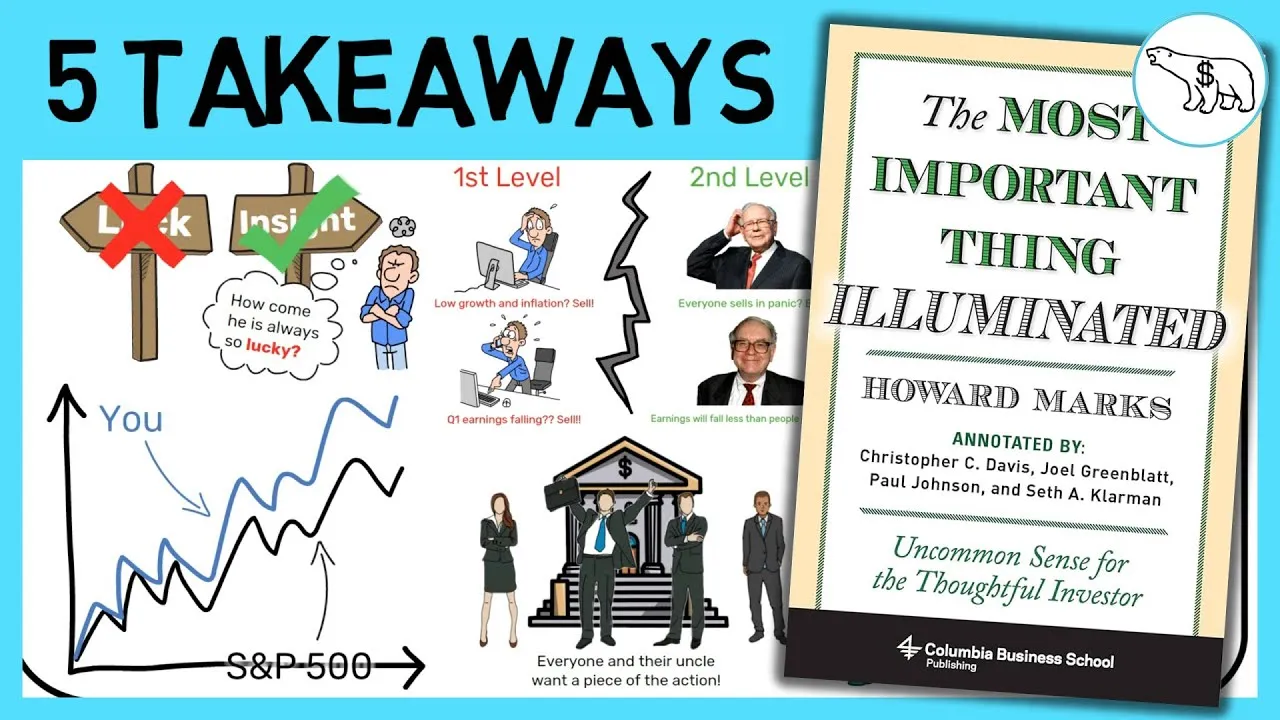

1. Identify Undervalued Niches: ‘Fish in the Right Pond’

Marks advocates for a contrarian approach to investment selection, urging investors to look beyond the hype. When popular assets like Tesla, as cited in the analysis, are trading at sky-high valuations, often priced to perfection with little room for upside surprises, it signals a less opportune time to buy. Instead, Marks suggests that superior investment opportunities arise from identifying assets that sellers are motivated to offload, rather than fixating on a predetermined list of desired holdings.

This strategy involves actively seeking out less obvious investment avenues. These ‘right ponds’ can include:

- Under-the-Radar Companies: Lesser-known or misunderstood businesses, such as corporate spin-offs or smaller enterprises, often fly beneath the market’s radar, presenting opportunities to uncover undervalued assets.

- Outdated or Niche Industries: Sectors perceived as declining, like cash transit services (exemplified by Loomis), can offer unique value precisely because they are overlooked by the broader market.

- Controversial or ‘Scary’ Investments: Assets linked to controversial themes such as oil, defense, or even gambling, may be mispriced due to negative sentiment. Marks suggests that stocks with perceived ‘defects’ or unpopular associations can trade at a discount relative to their intrinsic value, offering a higher return for the risk taken.

The core principle here is to find situations where pessimism has driven prices below fundamental value, creating a margin of safety and potential for significant upside.

2. Cultivate ‘Second-Level Thinking’

To achieve returns that outperform the market, investors need more than just luck; they require superior insight. Marks terms this deeper level of analysis ‘Second-Level Thinking.’ While first-level thinkers might react simplistically to market conditions—for instance, selling stocks during periods of low growth and high inflation—second-level thinkers delve deeper.

They consider the broader implications and potential market reactions. For example, a first-level thinker might sell a stock if earnings are expected to fall.

A second-level thinker, however, might buy, anticipating that the earnings decline will be less severe than the market expects, leading to a positive stock price surprise. This involves asking ‘and then what?’ to understand the consequences of consequences, a concept echoed by Warren Buffett and Charlie Munger.

Applying this to current trends, such as the enthusiasm around Artificial Intelligence (AI), a second-level thinker would consider not only the potential of AI but also the inevitable surge in valuations and competition that such a ‘golden opportunity’ attracts. The key is to identify where the market is currently exhibiting excessive fear or greed, and to act accordingly.

3. Acknowledge the Limits of Knowledge: ‘Know What You Don’t Know’

Marks cautions against the hubris of attempting to predict macroeconomic trends with certainty. He famously quotes, “There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” While engaging in macroeconomic discussions can be intellectually stimulating, relying on such predictions for investment decisions is often a path to underperformance.

Many macroeconomic factors are either unimportant or unknowable. Attempting to forecast short-term interest rate movements, for instance, is notoriously difficult, yet crucial for leveraged bets.

While exceptional investors like Michael Burry have made prescient calls, such instances are rare. Accurately predicting one major event does not guarantee success in forecasting subsequent market movements, like the rebound following the 2008 crisis.

Echoing the sentiment of investment stalwarts like Warren Buffett and Charlie Munger, Marks emphasizes focusing on what is knowable and important at the micro-level. This includes deeply understanding a company’s valuation relative to its peers, its cash flow generation efficiency, and the sustainability of its competitive advantages. Mastering these granular details offers a far greater return on analytical effort than speculative macroeconomic forecasting.

4. Evaluate Performance Holistically: The ‘Red Pill or Blue Pill’ Choice

When assessing investment performance, simply looking at headline returns, such as a high Compound Annual Growth Rate (CAGR), can be misleading. Marks, through the analogy of choosing between a ‘red pill’ (seeking deeper truth) and a ‘blue pill’ (accepting comfortable assumptions), urges investors to look beyond the surface.

A high return achieved with excessive risk is not necessarily superior. Just as a faster car journey might involve dangerous driving, a high CAGR could stem from concentrated bets, excessive leverage, or simply riding a market wave without true understanding. True investment skill, or ‘alpha,’ is demonstrated when returns are generated independent of broad market movements and are achieved with controlled risk.

Key indicators to scrutinize when evaluating an investor’s track record include:

- Portfolio Diversification: Returns heavily concentrated in a single stock or sector may indicate luck rather than skill.

- Leverage: High leverage can amplify gains but also magnifies losses, potentially leading to ruin (multiplying by zero).

- Performance During Market Downturns: A hallmark of skilled investing is resilience. Aggressive investors should ideally see their portfolios decline less than the market during downturns, while defensive investors should outperform during market crashes.

The true test of an investor’s mettle lies not just in the returns achieved, but in the risk taken and the consistency of performance across different market cycles.

5. Prioritize Capital Preservation: ‘Play to Not Lose’

Marks draws a parallel between professional tennis players and amateur ones to illustrate a crucial investment philosophy: play to not lose. Professional players aim for aggressive, winning shots. Amateur players, however, have a higher probability of success by focusing on keeping the ball in play and waiting for their opponent to make a mistake.

In investing, this translates to a defensive strategy focused on avoiding significant losses. While some investors aim for exceptional gains, Marks, and by extension investors like Warren Buffett, prioritize capital preservation. This means operating within one’s circle of competence, avoiding frothy valuations, eschewing excessive leverage, maintaining diversification, and insisting on a substantial margin of safety.

The rationale is that in investing, unlike in tennis where precise execution guarantees outcomes, randomness and unforeseen events (management errors, regulatory changes, disruptive innovation) can derail even the best-laid plans. Therefore, while offense can lead to riches, an exclusive focus on offense increases the risk of catastrophic failure. A defensive approach, characterized by risk aversion and a focus on avoiding losers, allows winners to compound over time, leading to wealth accumulation, albeit perhaps at a less spectacular pace.

Marks advises investors to “invest scared,” acknowledging the possibility of loss and the limits of their own knowledge. This cautious mindset prevents hubris and ensures a constant vigilance for potential risks, thereby safeguarding capital and fostering long-term success.

Market Impact

Howard Marks’ philosophy, as detailed in ‘The Most Important Thing,’ offers a robust framework for investors seeking to navigate volatile markets. By emphasizing the identification of undervalued assets in overlooked sectors, the cultivation of deep, second-level thinking, and a profound respect for the limits of predictability, investors can move beyond speculative trading.

The focus on holistic performance evaluation, considering risk alongside return, and prioritizing capital preservation through a defensive strategy provides a blueprint for sustainable wealth creation. In a time often dominated by short-term narratives and speculative fervor, Marks’ timeless wisdom is a critical reminder of the enduring principles that underpin successful long-term investing.

Source: THE MOST IMPORTANT THING SUMMARY (BY HOWARD MARKS) (YouTube)