11-Year Portfolio Outperforms Indices, Value Investor Shares Top Picks

A seasoned investor, with an impressive track record spanning over a decade, has revealed six companies selected for their buy-and-hold potential over the next six months. The investor, who has consistently beaten both the S&P 500 and the DJ World indices, shared insights into his portfolio’s performance and his updated investment strategy, which now involves less frequent, but more impactful, portfolio reviews.

Exceptional Long-Term Performance

Since commencing his investment journey in August 2013, the investor’s portfolio has delivered remarkable returns. According to his broker’s estimates, his compounded annual growth rate (CAGR) stands at 16%, significantly outperforming the S&P 500’s 11% and the DJ World’s 6.5% over the same period.

When calculated using Internal Rate of Return (IRR), the investor claims an even more substantial outperformance, with his own estimates reaching up to 19% annually. These figures are net of fees and taxes.

Resilient Recent Performance Amidst Challenges

Despite a challenging year for small and micro-cap stocks, which have historically underperformed in bull markets and were further impacted by a significant scam in one of their largest holdings, Kindred, the investor’s portfolio managed to post a gain of 17.4% (or 18.5% by his own calculation). This performance edged out the S&P 500’s 15.2% and the DJ World’s 11.7% for the past year. While pleased with the absolute returns, the investor noted that the efficiency of these returns required approximately 15 times more effort than in previous years.

Strategic Shift: Less Frequent, High-Impact Reviews

To address the increased effort and time commitment, the investor is reverting to a strategy of evaluating the portfolio every six months. This approach aims to maintain similar performance levels while freeing up significant time and simplifying the tracking process for investors. The goal is to implement major portfolio adjustments only when necessary during these semi-annual reviews.

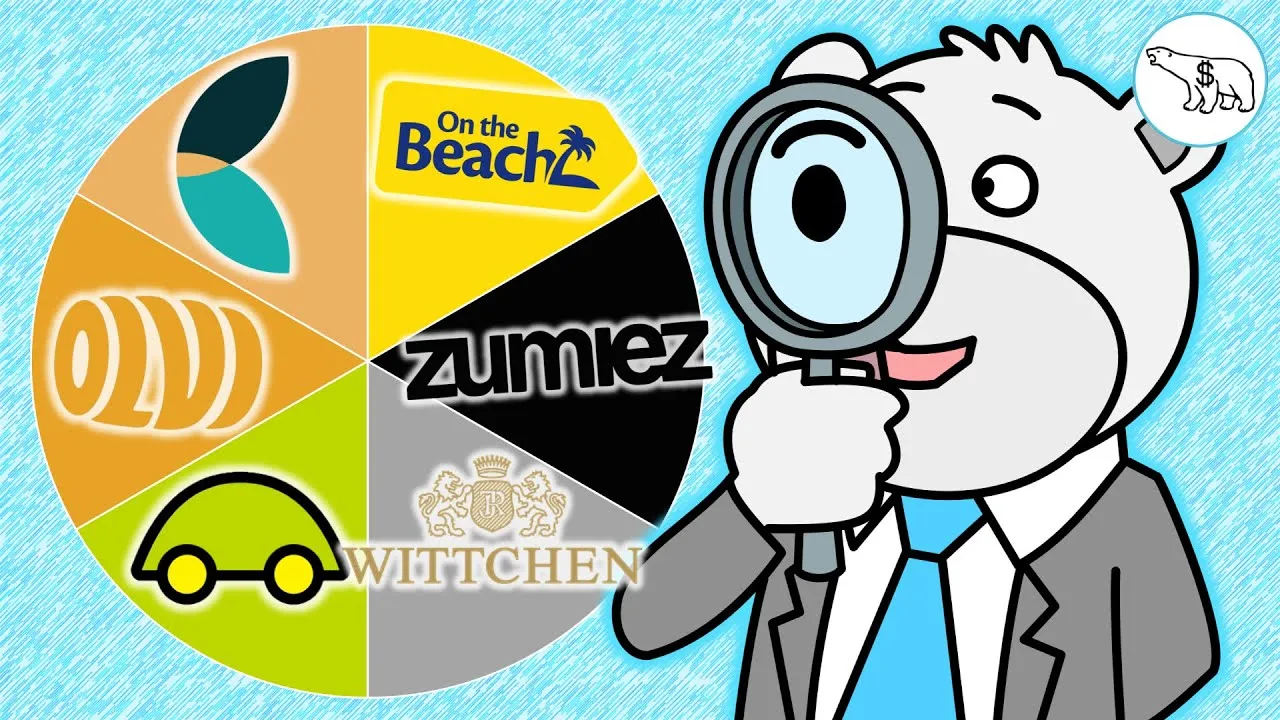

Portfolio Reveal: Six Companies for the Next Six Months

As part of this new transparency initiative, the investor has decided to reveal approximately half of his portfolio holdings. These six companies have been identified as strong candidates for a buy-and-hold strategy over the coming six months:

1. Carum (Healthcare Services)

Carum, a Swedish provider of healthcare services for the elderly, offers hardware devices for home monitoring and personal safety, connected to response centers. The business model is characterized by non-cyclicality and recurring revenues, serving a wide customer base in Sweden, Norway, and the UK. Carum is a market leader in Sweden and the UK, which constitute 60% of its sales.

- Growth & ROIC: Expected high single-digit organic growth with a Return on Invested Capital (ROIC) around 30%.

- Business Quality: Rated 4 out of 5, indicating a strong ability to retain customers and profits (a small ‘hole in the bucket’).

- Valuation: Trades at an Enterprise Value to EBITDA (EV/EBIT) of 13.37 and a Price-to-Earnings (P/E) of 16.8. Adjusted for amortization, the EV/EBIT falls to 10.9 and P/E to 12.5, considered attractive for a quality business.

2. Zumies (Skate Fashion Retailer)

Zumies is an American retailer specializing in skate fashion and accessories, with a global presence across the US, Canada, Europe, and Australia. While growth in the US is nearing saturation, opportunities for store expansion exist in Europe and Australia. The company has experienced recent headwinds due to weak customer demand, leading to a turnaround situation.

- Growth: Mid-single-digit organic growth is anticipated, driven by store expansion and inflation.

- ROIC: Approximately 20% in a normal year.

- Business Quality: Rated lower due to cyclicality and recent demand weakness, but considered a potential turnaround play.

- Valuation: Currently trades at EV/EBIT of 6.6. Historically, the company has been valued around EV/EBIT 10, suggesting potential upside if it returns to profitability. Zumies has no debt and a significant cash reserve.

3. Wojas (Footwear and Accessories)

Wojas is a Polish company manufacturing, marketing, and selling suitcases, bags, clothing, and accessories under the Wojas brand. It is an owner-operated business, with the founders holding a 60% stake. Sales are split between Poland and online channels.

- Growth: Short-term growth is expected to be subdued due to tough comparables from 2023’s post-COVID rebound. However, long-term low double-digit growth is projected, with the company gaining market share.

- ROIC: Expected to remain around 30%.

- Business Quality: Rated 3.5 out of 5, benefiting from its own brand and a nearly 10% market share in key categories, but facing intense competition and cyclicality.

- Valuation: Trades at a P/E of 10 and EV/EBIT of 8.5 on a last 12 months basis, considered inexpensive compared to similar companies in the US.

4. Komju (Used Car Retailer)

Komju is a Finnish retail company operating in the used car market, with showrooms in Finland, Sweden, and Germany. The business model involves acquiring, refurbishing, and reselling vehicles. Komju is the market leader in Finland but is currently operating its Swedish and German operations at a loss.

- Growth: Expected to slow to mid-single digits, with a focus on profitability over aggressive expansion.

- ROIC: Maintained at 20%.

- Business Quality: Rated 2.5 out of 5 due to competition and challenges in achieving profitability in new markets, coupled with industry cyclicality.

- Valuation: Trades at EV/EBIT of 8 and P/E of 8.5, considered very cheap, especially if the company can achieve its target of a 3.5% operating margin.

5. Olvi (Beverage Company)

Olvi is a leading beverage company in Finland, the Baltics, and Belarus, known for its localized beer brands. It operates in a non-cyclical industry with slow change and strong brand positioning.

- Growth: Organic volume growth of 4.5% annually, projected to reach around 6% including inflation.

- Business Quality: Rated 4.5 out of 5, benefiting from strong, localized brands and market leadership.

- Valuation: Trades at EV/EBIT of 8.9 and P/E of 11.5. A significant portion of its profits originates from Belarus, creating a geopolitical risk. However, even excluding Belarusian profits, the valuation of the remaining business is considered attractive, presenting an asymmetric bet.

6. On the Beach (Online Travel Retailer)

On the Beach is a UK-based online travel retailer specializing in vacation packages, including flights and accommodation. It operates with minimal capital requirements, leading to a near-infinite ROIC.

- Growth: Expected to grow at approximately 6% annually, following a strong post-2019 recovery.

- ROIC: Near infinite due to the asset-light business model.

- Business Quality: Rated 2 out of 5 due to potential winner-take-all dynamics, competition from giants like Booking.com, and the cyclical nature of holiday travel.

- Valuation: Trades at EV/EBIT of 9.7 and P/E of 9.1, considered inexpensive given its historical growth and operational efficiency.

Market Impact and Investor Considerations

The investor’s strategy emphasizes long-term value creation through diligent stock selection. The focus on companies with strong business fundamentals, reasonable valuations, and clear growth drivers, even within challenging market segments like small and micro-caps, offers a blueprint for investors seeking to outperform.

The shift to semi-annual reviews highlights a pragmatic approach to managing an investment portfolio efficiently. Investors considering these types of companies should be aware of the inherent risks associated with small and micro-caps, cyclical industries, and specific geopolitical or competitive challenges, as outlined for each company.

“The closer we are to danger, the farther we are from harm.” This philosophy highlights the approach to identifying opportunities in companies facing temporary difficulties but possessing resilient underlying businesses.

The investor also noted that these six companies represent smaller positions in his overall portfolio, with larger, more significant holdings detailed on his Patreon page, which has recently reduced its subscription price to $10 per month.

Source: 6 Stocks for the Buy & Hold in 2024 (+Patreon Update) (YouTube)