Seth Klarman’s seminal 1991 book, “Margin of Safety,” continues to resonate with investors, despite being out of print and commanding prices upwards of $2,000 for a physical copy. The enduring demand for this guide to risk-averse value investing, penned by the legendary investor behind the $25 billion Baupost Group, highlights its timeless relevance. While the reasons for a lack of a second edition remain speculative, the core tenets of Klarman’s philosophy offer invaluable insights for navigating financial markets.

Value Investors vs. Speculators: A Fundamental Divide

Drawing heavily from the foundational principles of Warren Buffett and Benjamin Graham, Seth Klarman distinguishes sharply between value investors and speculators. This distinction, central to his approach, hinges on the source of perceived value.

Value investors, according to Klarman, focus on a business’s intrinsic worth, particularly its cash flows and the potential for future earnings. They seek to acquire securities when their price is significantly below their estimated underlying business value, and divest when this discount disappears.

In contrast, speculators prioritize market price movements. Their investment decisions are driven by anticipated fluctuations in security prices, often based on what they believe other market participants will do. This approach is inherently riskier, as it relies on predicting future price action rather than assessing the fundamental economics of a business.

Klarman likens assets that do not produce anything of value or cash flow—such as art, antiques, rare coins, or even cryptocurrencies in this context—to pure speculation. Their value is derived solely from the expectation that a future buyer will pay a higher price, a cycle that is unsustainable and precarious.

True investments, for a value investor, are assets that generate tangible cash flows. This includes businesses that produce goods or services people want, real estate that yields rent, software companies with recurring subscription revenues, or loans that generate interest. The key is to acquire these cash-flowing assets at a price that is reasonable relative to their current cash generation, their potential for growth, and, crucially, the risk that these cash flows might diminish.

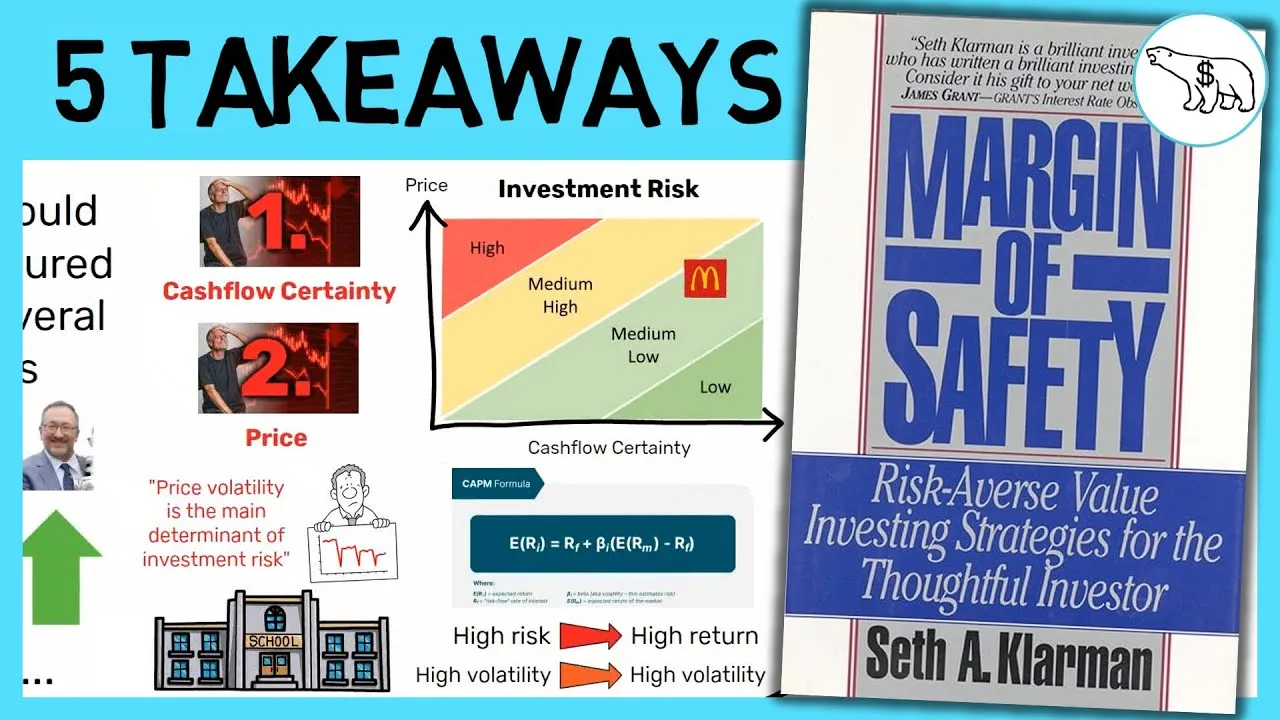

Understanding Investment Risk: Beyond Beta

The concept of investment risk is often misunderstood, and Klarman dedicates significant attention to clarifying it. He aligns with Warren Buffett’s adage to “never lose money” not by avoiding all market downturns, but by ensuring that over the long term, material losses are avoided. For value investors, risk is a dual-sided equation: it is determined by both the inherent nature of the asset being purchased (its cash flow certainty) and the price paid for it.

A company with a long operating history in a stable industry, like McDonald’s, might offer highly predictable cash flows, thus scoring well on the first criterion. However, if its stock trades at a very high valuation multiple (e.g., a Price-to-Earnings ratio of 32 or Enterprise Value-to-EBIT of 25), the price paid introduces significant risk. An investor could still lose money if market sentiment shifts and the valuation multiple contracts, even if the business itself remains sound.

Klarman strongly criticizes financial academics and many Wall Street professionals who equate investment risk primarily with price volatility, often measured by Beta. The Capital Asset Pricing Model (CAPM), which suggests higher returns are compensation for higher risk, is a prime example of this flawed thinking.

Klarman argues that risk, in fact, erodes returns through potential losses. Price volatility alone fails to account for the fundamental characteristics of the asset and its price, making it an inadequate measure of true investment risk.

Valuation Methods: Finding Intrinsic Worth

Determining the intrinsic value of a security is paramount for a value investor. Klarman outlines three primary methods:

- Liquidation or Breakup Value: This method involves assessing the net value of a company’s assets if it were to be dissolved. By summing all assets and subtracting liabilities, one arrives at a theoretical liquidation value. While many profitable businesses are not intended for liquidation, this can serve as a valuable “floor” or “cushion,” especially if the assets are tangible and easily convertible to cash. In instances where a company trades below the net value of its assets, it may present an attractive opportunity.

- Stock Market Value: This approach involves comparing a company’s valuation metrics (like P/E or EV/EBIT) to those of similar companies or industry averages. For example, if a semiconductor firm trades at a P/E of 20 while the industry average is 30, it might suggest potential upside through multiple expansion. However, Klarman cautions that the entire market or industry can be mispriced, making this method most reliable in specific situations like spin-offs.

- Discounted Cashflow (DCF) Analysis: This theoretically sound method involves projecting future cash flows and discounting them back to their present value using an appropriate discount rate. It is most effective for businesses with predictable future prospects. However, its accuracy is highly sensitive to assumptions about growth rates and other future variables, making it susceptible to the “garbage in, garbage out” problem.

Often, a combination of these methods provides the most robust valuation, particularly for complex, diversified businesses. The ultimate goal of any valuation exercise is to identify a price significantly below the calculated intrinsic value, thereby establishing a margin of safety.

The Role of Cash and Opportunity Cost

The decision of whether to remain fully invested or hold cash is a nuanced aspect of investing, deeply tied to the concept of opportunity cost. Opportunity cost, in investing, means that by allocating capital to one asset, an investor forfeits the potential gains from other opportunities. Klarman introduces another dimension: the opportunity cost of not holding cash during market downturns.

While being fully invested can be detrimental if the market plunges, holding excessive cash also carries an opportunity cost, especially if the market rallies. Klarman suggests a middle ground: instead of simply sitting in cash, investors can position themselves to have capital available at opportune times by investing in assets that are likely to return cash in the near future. Examples include high-dividend-paying stocks (where dividends can be reinvested at lower prices), companies undergoing liquidation, or merger arbitrage situations where capital is returned relatively quickly.

This strategy allows investors to avoid being completely on the sidelines during a downturn while still preparing for potential market bottoms. The principle is that money is not lost but transferred; by having capital ready to deploy, investors can capitalize on market dislocations.

The 80/20 Approach to Idea Generation

Klarman advocates for an 80/20 approach to investment research, suggesting that investors should spend the majority of their time evaluating a broad range of opportunities rather than delving excessively deep into a few. This contrasts with the common tendency to meticulously research minor purchases while making significant investment decisions impulsively.

The rationale is that truly exceptional investment opportunities—those with a clear and substantial margin of safety—often present themselves as “screaming buys” that require less intensive due diligence. By sifting through a large number of potential investments, investors increase their chances of spotting these obvious opportunities. Even time spent investigating ideas that are ultimately rejected is not wasted, as the knowledge gained is cumulative and can prove valuable in the future.

Market Impact

Klarman’s philosophy, emphasizing value investing principles, risk mitigation, and a disciplined approach to valuation, offers a counterpoint to speculative market behavior. In a time often characterized by rapid price movements and thematic investing, his focus on intrinsic value and downside protection remains a bedrock for long-term wealth creation.

The emphasis on a margin of safety is particularly critical when market valuations appear stretched, serving as a crucial buffer against unforeseen events and market irrationality. The principle of understanding risk beyond mere volatility is essential for investors seeking to avoid costly mistakes, especially in sectors prone to speculative bubbles or rapid technological shifts.

What Investors Should Know

For investors, the enduring lessons from “Margin of Safety” are clear:

- Prioritize a business’s cash flows and underlying value over short-term price fluctuations.

- Understand that true investment risk is a combination of asset quality and purchase price, not just price volatility.

- Employ multiple valuation methods to determine a security’s intrinsic worth and always seek a margin of safety.

- Manage cash strategically to avoid opportunity costs, both from being fully invested in a falling market and from holding too much cash during a bull run.

- Adopt an efficient research process, focusing on broad idea generation to increase the likelihood of finding compelling opportunities.

By adhering to these principles, investors can build a more resilient and potentially more profitable portfolio, grounded in fundamental analysis and a deep respect for risk.

Source: MARGIN OF SAFETY SUMMARY (BY SETH KLARMAN) (YouTube)