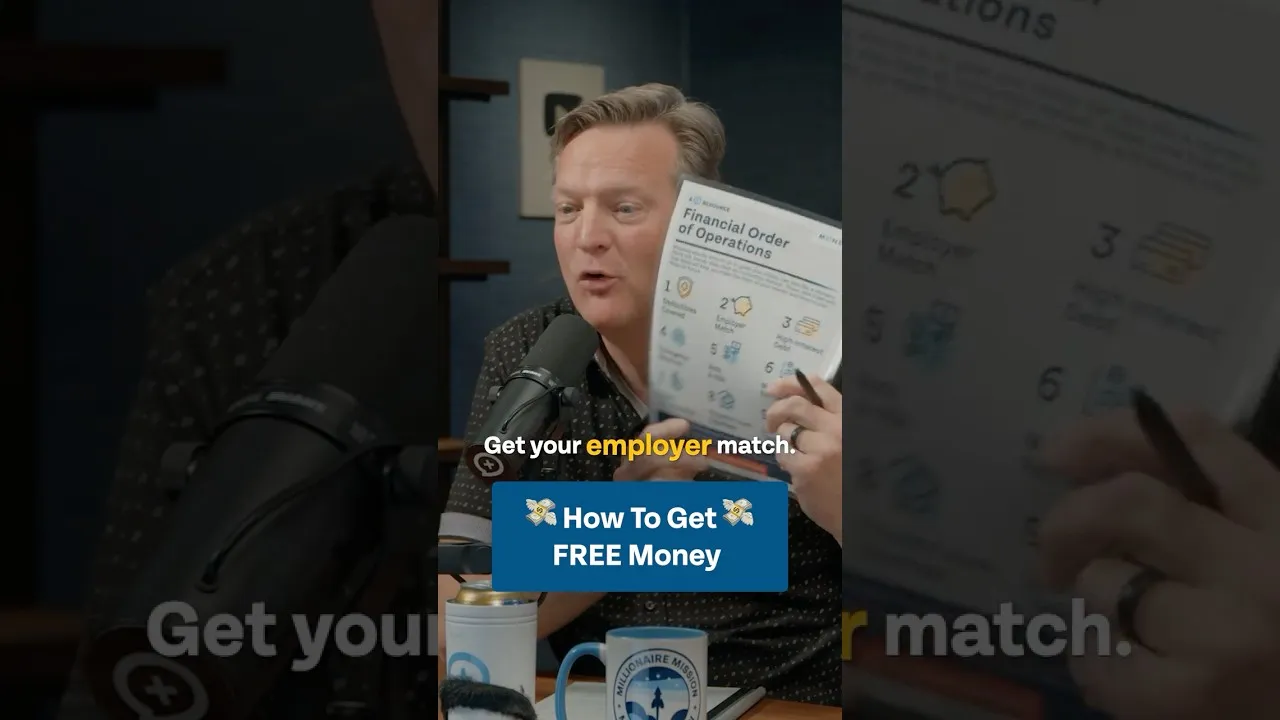

Employer Match: The First Step to Tax-Free Wealth Accumulation

In the intricate landscape of personal finance, prioritizing employer-sponsored retirement plans, specifically securing the full employer match, stands as a critical, often overlooked, initial step. This strategy, often termed the “financial order of operations,” offers a dual benefit: immediate financial uplift through free capital and significant long-term tax advantages. For many individuals, simply contributing enough to their 401(k) or similar plan to capture the entirety of their employer’s matching contribution is akin to receiving “free money,” a powerful catalyst for wealth building.

The Power of the Employer Match

Employer matching contributions are essentially free funds provided by your employer when you contribute to your retirement account. For instance, an employer might offer to match 50% of your contributions up to 6% of your salary.

This means if you contribute 6% of your income, your employer adds an additional 3%, effectively increasing your total contribution by 50% instantly. This immediate boost significantly accelerates the growth potential of your retirement savings.

Failure to secure the full employer match is akin to leaving a portion of your salary on the table. This lost opportunity can have a substantial negative impact on your long-term financial health, as it reduces the principal amount that can benefit from compounding returns over time.

Prioritizing Tax-Advantaged Accounts

Once the employer match is secured, the next strategic move involves prioritizing contributions to tax-advantaged accounts. These accounts, such as Roth IRAs, Roth 401(k)s, and Health Savings Accounts (HSAs), offer distinct benefits that enhance wealth accumulation.

Roth Accounts: Tax-Free Growth and Withdrawals

Roth IRAs and Roth 401(k)s operate on an after-tax contribution basis. While you don’t receive an immediate tax deduction for your contributions, the principal and earnings grow tax-deferred. The most significant advantage emerges during retirement: qualified withdrawals from these accounts are entirely tax-free.

This means that every dollar you withdraw in retirement, including all the accumulated earnings, is not subject to federal or state income taxes. This tax-free income stream can be invaluable, especially if you anticipate being in a higher tax bracket during your retirement years.

Health Savings Accounts (HSAs): A Triple Tax Advantage

Health Savings Accounts (HSAs) offer a unique triple tax advantage. Contributions made to an HSA are typically tax-deductible, lowering your current taxable income. The funds within the HSA grow tax-deferred, similar to traditional retirement accounts.

Finally, qualified withdrawals for medical expenses are tax-free. After age 65, HSA funds can be withdrawn for any purpose, not just medical expenses, and will be taxed as ordinary income, much like a traditional IRA or 401(k). This flexibility makes HSAs a powerful tool for both healthcare cost management and long-term retirement savings.

The Financial Order of Operations

The recommended sequence for maximizing your financial potential is often outlined as follows:

- Step 1: Build an emergency fund.

- Step 2: Contribute enough to your employer’s retirement plan to receive the full match.

- Step 3: Prioritize contributions to tax-advantaged accounts like Roth IRAs, Roth 401(k)s, and HSAs.

- Step 4: Pay down high-interest debt.

- Step 5: Invest above and beyond your tax-advantaged accounts in taxable brokerage accounts.

By adhering to this order, individuals ensure they are capitalizing on the most advantageous financial opportunities first, building a robust foundation for long-term financial security.

Market Impact and Investor Considerations

The strategy of prioritizing employer matches and tax-advantaged accounts has profound implications for individual investors and the broader market. By directing capital into these vehicles, individuals not only enhance their personal financial outlook but also contribute to the pool of long-term investment capital. The tax benefits associated with these accounts encourage sustained investment, providing a stable source of funding for businesses and economic growth.

Short-Term Implications:

- Increased Savings Rate: Actively pursuing employer matches necessitates a higher personal savings rate, which can impact immediate discretionary spending but builds future financial resilience.

- Tax Benefits Realization: While Roth contributions don’t offer an upfront deduction, the immediate tax-free growth is a powerful incentive. For HSAs, the upfront tax deduction provides immediate savings.

Long-Term Implications:

- Compounding Power: The tax-deferred and tax-free growth environments allow for more powerful compounding over extended periods, leading to significantly larger retirement nest eggs.

- Tax Diversification: Holding assets in various tax buckets (taxable, tax-deferred, tax-free) provides flexibility in retirement planning, allowing for strategic withdrawal management to minimize tax liabilities.

- Reduced Retirement Risk: A substantial tax-free income stream in retirement reduces the overall financial risk associated with market volatility and unexpected expenses.

For investors, understanding and implementing this financial order of operations is not merely about saving; it’s about strategically deploying capital to maximize returns and minimize tax burdens. The “free money” from employer matches acts as the initial leverage, while tax-advantaged accounts provide the engine for sustained, tax-efficient wealth accumulation. This disciplined approach forms the bedrock of sound long-term financial planning.

Source: Don’t Skip This “Free Money” Step (YouTube)