Financial Experts Scrutinize Social Media’s Money Advice

In a world saturated with quick financial tips and ‘money hacks’ from platforms like TikTok and YouTube, seasoned financial advisors are stepping in to dissect the validity and impact of this readily available advice. A recent analysis of popular online content reveals a spectrum of financial guidance, ranging from sound, albeit sometimes misunderstood, strategies to potentially detrimental shortcuts. The core debate often centers on the definition and practice of frugality, with experts emphasizing the crucial difference between being financially prudent and excessively miserly.

Frugality: A Tool, Not a Punishment

One common theme emerging from social media discussions is the public’s perception of frugality. Advisors highlighted instances where individuals were criticized for enjoying quality goods or hiring help, such as a nanny, under the guise of being ‘frugal.’ The consensus among the financial experts is that frugality is not about deprivation but about mindful spending and prioritizing value.

“Frugality isn’t about deprivation and not being able to enjoy luxuries that add value to your life. I budget for a nanny. Because I value being able to have time for myself, to focus on my passion projects, and it’s within our means.”

Similarly, purchasing items on clearance, a strategy often lauded by financial gurus, has drawn criticism online, with some suggesting it deprives those in genuine need. However, financial professionals argue that smart shopping and utilizing discounts are fundamental to wealth accumulation. The key, they stress, is mindful consumption – buying what you need and can afford, rather than hoarding or taking essentials meant for others.

The ‘buy nothing’ groups also came under scrutiny. While the intention is to share and reduce waste, advisors noted that participating should involve giving more than taking, especially by prioritizing essential items for those who truly need them.

Investment Vehicles for the Risk-Averse

The discussion also delved into investment strategies, particularly for middle-class Americans who are risk-averse. While Treasury Inflation-Protected Securities (TIPS) were mentioned as a way to guarantee a real return, experts cautioned against viewing them as the sole solution for all risk-averse investors.

The prevailing advice leaned towards diversified portfolios, especially for younger investors. Funds that track broad market indexes, such as the S&P 500 or total stock market index funds, were recommended for their long-term growth potential. For those seeking even more defined risk management, a closed-ended target-date retirement index fund was suggested, offering a blend of equities and fixed income that adjusts over time.

The debate touched upon the idea that any investment seeking a return beyond inflation inherently involves some level of risk. The emphasis remained on diversification and a long-term perspective, with index funds and target-date funds being highlighted for their ability to provide this balance without excessive fees, particularly from providers like Fidelity, Vanguard, and Charles Schwab.

Navigating the Housing Market: Affordability vs. Qualification

A significant portion of the analysis focused on housing affordability, using the example of a $300,000 home for an individual earning $75,000 annually. The calculations showed that while a borrower might technically qualify based on a 40% debt-to-income ratio, the resulting monthly payment consumed 57% of their take-home pay.

Financial experts strongly advised against such scenarios, labeling them as ‘house-rich, life-poor.’ They advocated for stricter affordability guidelines, such as the 35/25 rule (3% down payment, no more than 25% of gross income for total housing costs, and intending to stay in the home for at least 5 years). The advice underscored the importance of not just qualifying for a loan but comfortably affording the payments without jeopardizing other financial goals.

The discussion also acknowledged the potential for income growth. For individuals on an upward income trajectory in stable fields, stretching affordability might be manageable. However, the underlying principle remains: personal financial situations are unique, and rigid rules like the 35/25 guideline provide a crucial grounding.

The ‘Latte Effect’ and Spending Habits

The popular concept of the ‘latte effect’—where small, daily discretionary purchases like a $5 coffee can add up significantly over time—was thoroughly examined. While some social media users dismiss its importance, financial advisors generally agree that for those starting their financial journey, monitoring these small expenses is crucial.

The experts differentiated between being frugal and being a ‘miser.’ For individuals building their financial foundation, cutting back on non-essential daily purchases, like an expensive daily coffee, can free up substantial amounts—potentially $150 or more per month—to be directed towards savings and investments. This disciplined approach helps avoid the ‘consumption trap’ and builds wealth.

However, as individuals achieve financial security and progress through wealth-building stages, the strict adherence to every small expense can become less critical. The key is to find a balance.

Enjoying a cup of coffee, if it aligns with personal values and doesn’t derail financial goals, is acceptable. The advice shifts from meticulous budgeting to cash management, allowing for enjoyment of life’s pleasures without regret once foundational financial goals are met.

“The latte effect is very important when you first start out on your journey. You should be watching where your money goes, even on little things like coffee when you’re starting out. By the time you get to level three of the five levels of wealth, which is security, you don’t have to sweat the small stuff anymore.”

Long-Term Wealth Building: Early and Consistent Saving

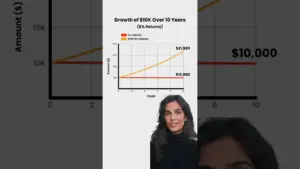

The power of starting early with retirement savings was powerfully illustrated through a comparison of two individuals receiving a $10,000 bonus. One invested a small portion immediately in a Roth IRA and planned to contribute sporadically, while the other prioritized consistent, early investment.

The stark difference in outcomes—one account growing to $178,000 tax-free over time, while the other remained significantly smaller—underscored the impact of compound growth and consistent contributions. The message was clear: while starting early is vital, continuous saving and investing are paramount for building substantial long-term wealth.

The ‘set it and forget it’ approach, often facilitated by automatic contributions to retirement accounts like Roth IRAs, was lauded as an effective strategy to mitigate market volatility and personal spending impulses. This automatic discipline is seen as a protective mechanism against both external market fluctuations and internal desires for immediate gratification.

Discerning Good from Bad Advice

Ultimately, the analysis of social media financial advice emphasizes the need for critical discernment. While many platforms offer valuable insights, users must differentiate between sound financial principles and potentially harmful or misleading information. Financial professionals encourage viewers to utilize reliable resources and understand that personal finance is, indeed, personal.

Market Impact & Investor Takeaways

- Frugality vs. Miserliness: True frugality involves mindful spending and prioritizing value, not self-deprivation. Avoid falling into the trap of being a ‘miser’ at the expense of quality of life once financial goals are met.

- Investment Strategy: For risk-averse investors, diversified index funds (like S&P 500 or total market) and target-date retirement funds offer a balanced approach for long-term growth.

- Housing Affordability: Go beyond loan qualification; ensure housing payments are comfortably affordable within a conservative percentage of your gross income (e.g., 25%) to avoid financial strain.

- ‘Latte Effect’: While small purchases add up, their significance diminishes as one achieves financial security. Prioritize saving early, but allow for discretionary spending that enhances life quality later on.

- Compound Growth: The earlier and more consistently you invest, the greater the benefit of compound growth, especially in tax-advantaged accounts like Roth IRAs.

Source: Financial Advisors React to Money Advice on TikTok & YouTube (YouTube)