Key Takeaway: The Power of Tracking Small Expenses

A meticulously crafted budgeting spreadsheet, designed for simplicity and immediate input, is proving instrumental in helping individuals identify and curb excessive spending, particularly in areas like dining out and impulse purchases. This approach, focused on awareness rather than strict discipline, has demonstrated the potential to save individuals thousands of dollars annually by making the financial impact of small, frequent transactions immediately apparent.

The Silent Drain: Dining Out and Impulse Buys

The core of this budgeting strategy addresses a common financial pitfall: the cumulative effect of small, seemingly insignificant expenses. For many, especially those who work from home, the temptation to dine out or make convenience purchases can be a significant drain on finances.

These expenses, often ranging from $10 to $20 per outing, do not feel substantial individually but can escalate rapidly. The creator of the spreadsheet highlights this personal struggle, noting that the primary motivation for eating out was not a lack of cooking skills or financial inability, but a need to escape the confines of home and family.

“Why eating out is one of the worst budget categories is because it can be silent. Okay, these there’s small purchases. They don’t feel expensive at first, but they add up.”

This realization spurred the development of a straightforward tracking system. Unlike complex budgeting apps that require linking numerous accounts and involve intricate categorizations, this method prioritizes ease of use and immediate feedback. The principle is that by logging every expenditure the moment it occurs, individuals gain a powerful, real-time awareness of their spending habits.

The Spreadsheet Solution: Simplicity and Immediate Awareness

The budgeting spreadsheet is designed with a minimalist approach. Its effectiveness hinges on the user’s commitment to logging every single transaction immediately after it happens. This instant input is crucial.

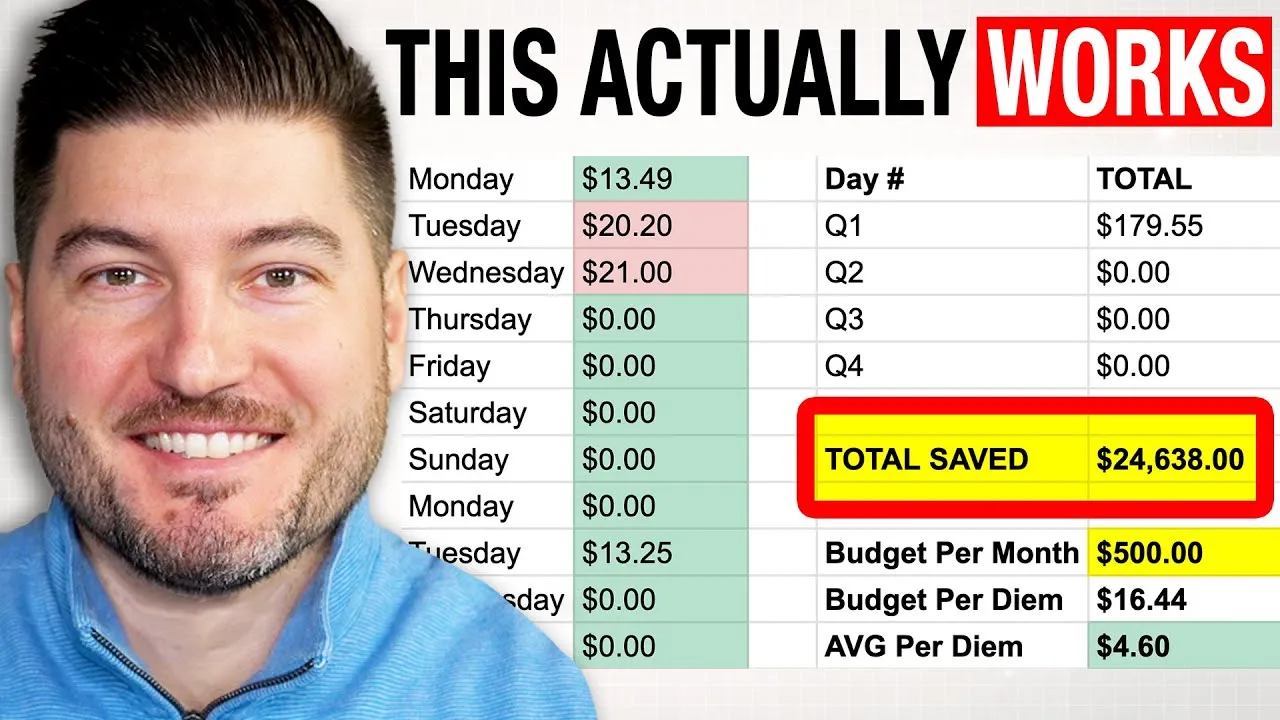

For instance, a $13.49 lunch purchase at a restaurant is logged directly into the spreadsheet. This immediate act of recording transforms a fleeting impulse into a tangible data point, prompting reflection.

The spreadsheet features a clear, color-coded system. A daily budget is established, and cells turn green if spending is below the daily threshold and red if it exceeds it. This visual cue is an immediate indicator of financial behavior.

The creator’s own experience showcases this: their daily average spend in the dining-out category is a mere $4.85, resulting in a monthly expenditure of approximately $147. This is a stark contrast to previous, unquantified spending habits that were significantly higher.

Beyond dining, the spreadsheet is adaptable to other problem spending areas, such as online shopping or retail therapy. A separate tab can be dedicated to these categories, allowing users to set monthly budgets for specific vices.

The key is consistent, real-time input. The act of opening a mobile app and entering a few digits after a purchase creates a pause, a moment of consideration that can deter impulsive decisions.

The Psychology of Tracking: What Gets Measured, Gets Managed

The underlying principle driving the spreadsheet’s success is the adage, “What gets measured gets managed.” By making every dollar spent visible and accountable, individuals are more likely to make conscious spending decisions. This is akin to the discipline required for calorie counting or tracking workout metrics; the act of measurement itself fosters accountability and encourages better choices.

The creator emphasizes that this system is not about deprivation but about awareness and intentionality. It doesn’t require immense willpower or complex financial acumen.

Instead, it leverages a simple behavioral loop: make a purchase, log the expense, reflect on the decision. This process can be as effective as a Pavlovian response, conditioning the user to think twice before spending.

The system’s long-term viability is attributed to its non-restrictive nature. Unlike traditional budgeting methods that can feel overwhelming or punitive, this approach focuses on tracking a specific area of concern. The visual feedback—green for good, red for cautionary—provides a clear, immediate understanding of progress without enforcing rigid rules that can lead to burnout.

Market Impact and Investor Considerations

While this budgeting tool is personal, its principles have broader implications for consumer spending patterns. A widespread adoption of such mindful spending habits could lead to shifts in consumer demand, particularly impacting sectors reliant on discretionary spending like restaurants, retail, and e-commerce. Companies that rely heavily on impulse purchases or convenience-driven sales might see slower growth if consumers become more intentional with their spending.

For investors, understanding consumer psychology and spending triggers is crucial. Tools that empower consumers to gain control over their finances can lead to increased savings rates, potentially redirecting funds towards investments or other financial goals. This could translate to higher capital available for investment in the long run, benefiting markets that cater to long-term wealth building.

The trend towards digital tools that simplify financial management, even if it’s a basic spreadsheet, indicates a growing demand for user-friendly financial solutions. Companies offering intuitive budgeting apps, personal finance management (PFM) tools, and investment platforms that integrate seamlessly into users’ lives are likely to capture market share.

What Investors Should Know

- Consumer Discretionary Spending: Be aware of how shifts in consumer behavior, driven by increased financial awareness and tracking, can impact sectors reliant on discretionary spending.

- Fintech Innovation: The demand for simple, effective financial tools highlights opportunities in the fintech space, particularly for platforms that offer intuitive user experiences and actionable insights.

- Savings Rate Trends: An increase in personal savings rates, potentially fueled by better budgeting practices, can free up capital for investment, influencing market liquidity and asset prices.

- Behavioral Finance: The success of this simple spreadsheet highlights the power of behavioral economics in financial decision-making. Tools that tap into psychological triggers for better financial habits are likely to resonate with consumers.

Long-Term Implications for Personal Finance

The spreadsheet’s success lies in its ability to foster lasting behavioral change. By making the consequences of spending immediately visible, it encourages a more thoughtful approach to consumption. This awareness can lead to sustained savings, improved financial health, and a greater capacity for long-term financial planning, such as investing for retirement or achieving other significant financial goals.

The creator suggests that this method is particularly beneficial for individuals who are analytical, appreciate visual feedback, and are willing to engage in a simple, consistent tracking process. While complex financial tools have their place, the power of this basic spreadsheet lies in its directness and its ability to provide immediate, actionable insights that can fundamentally alter spending habits for the better, saving thousands of dollars annually.

Source: The Only Budgeting Spreadsheet You’ll Ever Need (Seriously) (YouTube)