Understanding Business Insurance When Disaster Strikes

Imagine opening your dream bakery. You pour your heart, soul, and savings into it, and it becomes a beloved local spot.

Then, unexpectedly, disaster strikes – perhaps a lightning strike causes a fire, and your bakery is destroyed. Without a safety net, rebuilding might seem impossible, leaving your entrepreneurial dreams in ashes.

This article will guide you through understanding business insurance, explaining how it acts as a financial “oven mitt” to protect your business from devastating losses. You’ll learn about the core concepts of insurance, including premiums, coverage, and the principle of risk pooling, and how these elements can help you recover and reopen even after a catastrophic event.

What is Business Insurance?

Fundamentally, business insurance is a financial tool designed to protect your business from unforeseen events that could lead to significant financial loss. Think of it like an oven mitt for your finances. Just as an oven mitt allows you to handle hot objects without burning yourself, insurance allows your business to navigate potentially ruinous financial situations without suffering irreparable damage.

Key Concepts in Insurance

To understand how insurance works, it’s essential to grasp a few fundamental concepts:

Premiums: Your Investment in Protection

When you purchase an insurance policy, you agree to pay a regular amount of money to the insurance company. This payment is called a premium.

Premiums are typically paid annually, semi-annually, or monthly. By paying your premium, you are essentially buying financial protection against specific risks.

Coverage: The Scope of Your Protection

In exchange for your premium payments, the insurance company provides coverage. Coverage is the extent of the protection you receive under the policy.

It outlines what types of events or losses the insurance company will financially assist you with. Each policy is unique, detailing the specific risks covered and the limits of that coverage.

Risk Pooling: Strength in Numbers

You might wonder where the insurance company gets the money to pay for claims. The answer lies in the concept of risk pooling.

When you become an insurance policyholder, you join a larger group of individuals or businesses who also have policies with the same insurance company. Everyone in this group pays their premiums into a central fund.

This collective fund, or “pool,” is then used to pay out claims when a disaster strikes any member of the group. Since not everyone experiences a loss at the same time, the premiums paid by the many are sufficient to cover the costs for the few who do experience a covered event. This shared responsibility makes it possible for insurance companies to offer financial protection against large, unpredictable losses.

How Insurance Works in Practice: The Bakery Example

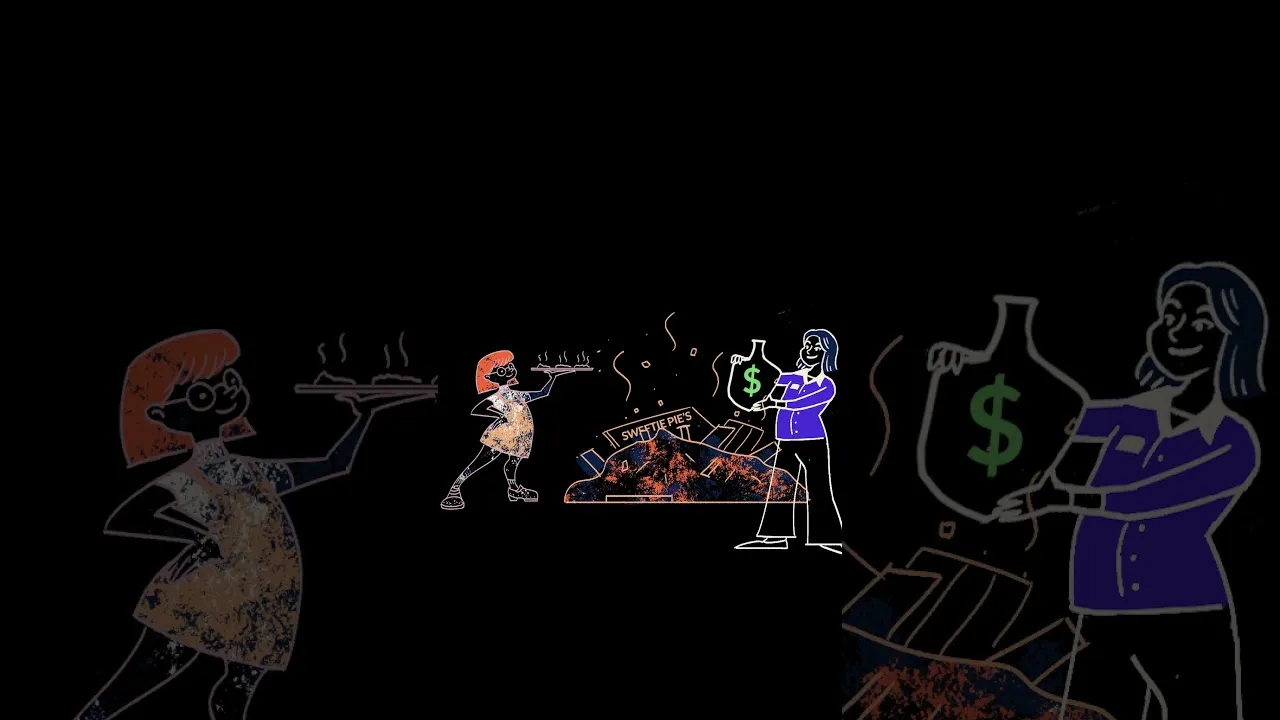

Let’s revisit the bakery scenario. Suppose your bakery has a comprehensive business insurance policy. One day, a severe thunderstorm rolls in, and lightning strikes your building, causing a fire that destroys the premises and much of your equipment.

Without insurance, you would face the daunting task of rebuilding from scratch with no financial support. However, with your insurance policy in place, you contact the insurance company.

They assess the damage, and because the fire was a covered event under your policy, they provide you with funds to help rebuild your bakery and replace your equipment. This allows you to reopen your business and continue serving your customers, turning a potential business-ending catastrophe into a manageable setback.

Factors Influencing Premiums: Risk Assessment

The cost of your insurance premium isn’t arbitrary. Insurance companies employ underwriters who assess the level of risk associated with insuring a particular business or individual. They evaluate how likely it is that a claim will be made.

Several factors influence this risk assessment:

- Location: A bakery located near an active volcano would be considered extremely high risk and might be uninsurable or command a very high premium due to the increased likelihood of a catastrophic event. Conversely, a bakery in a stable, low-risk area would likely have lower premiums.

- Industry and Operations: The type of business and its day-to-day operations also play a role. A business that handles flammable materials might face higher premiums than one that doesn’t.

- Safety Measures: Implementing safety protocols and having good security systems can sometimes lower premiums by reducing the perceived risk.

While the bakery example focused on property damage from a lightning strike, it’s important to remember that business insurance can cover a wide array of risks. These can include liability for accidents, theft, business interruption, and more, depending on the specific policies purchased.

Beyond Business Insurance

Business insurance is just one facet of the broader insurance landscape. Individuals and other types of businesses utilize various forms of insurance to protect against different risks:

- Health Insurance: Covers medical and surgical expenses.

- Dental Insurance: Covers dental care costs.

- Car Insurance: Covers damage to vehicles and liability from accidents.

- Life Insurance: Provides a financial payout to beneficiaries upon the insured’s death.

- Home Insurance: Covers damage to a home and its contents due to various perils.

Understanding these different types of insurance highlights the pervasive role they play in providing financial security and peace of mind in an unpredictable world.

Conclusion

Having the right business insurance is not just about protecting your physical assets; it’s about safeguarding your livelihood and the future of your business. By understanding premiums, coverage, and the principle of risk pooling, you can make informed decisions about the insurance policies that best suit your needs. When disaster strikes, a solid insurance policy can be the crucial difference between recovery and ruin, allowing your business to weather the storm and continue to thrive.

Source: Your Bakery Burns Down. Now What? Understanding Insurance (YouTube)