Parents Demand $114,000 Repayment for 529 Plan Funds

A recent revelation has sent shockwaves through the personal finance community as a young professional is being asked by her parents to repay nearly $114,000. This sum represents the entire balance of a 529 college savings plan that was established for her education. The situation highlights a complex interplay between parental financial support, investment growth, and the often-unspoken expectations surrounding educational funding.

The 529 Plan and Its Unexpected Terms

A 529 plan is a tax-advantaged savings plan designed to encourage saving for future education costs. Contributions grow tax-deferred, and withdrawals are tax-free when used for qualified education expenses. In this case, the parents had set up the plan early in their daughter’s life, and she utilized it to fund the majority of her undergraduate and graduate studies.

However, the expectation of this financial support has taken a sharp turn. The parents are now requesting the full $114,000 balance of the account be repaid. This figure represents not just the principal contributions made by the parents but also the accumulated compound growth over the years. Financial experts often point out that the growth within a 529 plan is a benefit of the investment strategy and the passage of time, not necessarily an additional cost to the account holder.

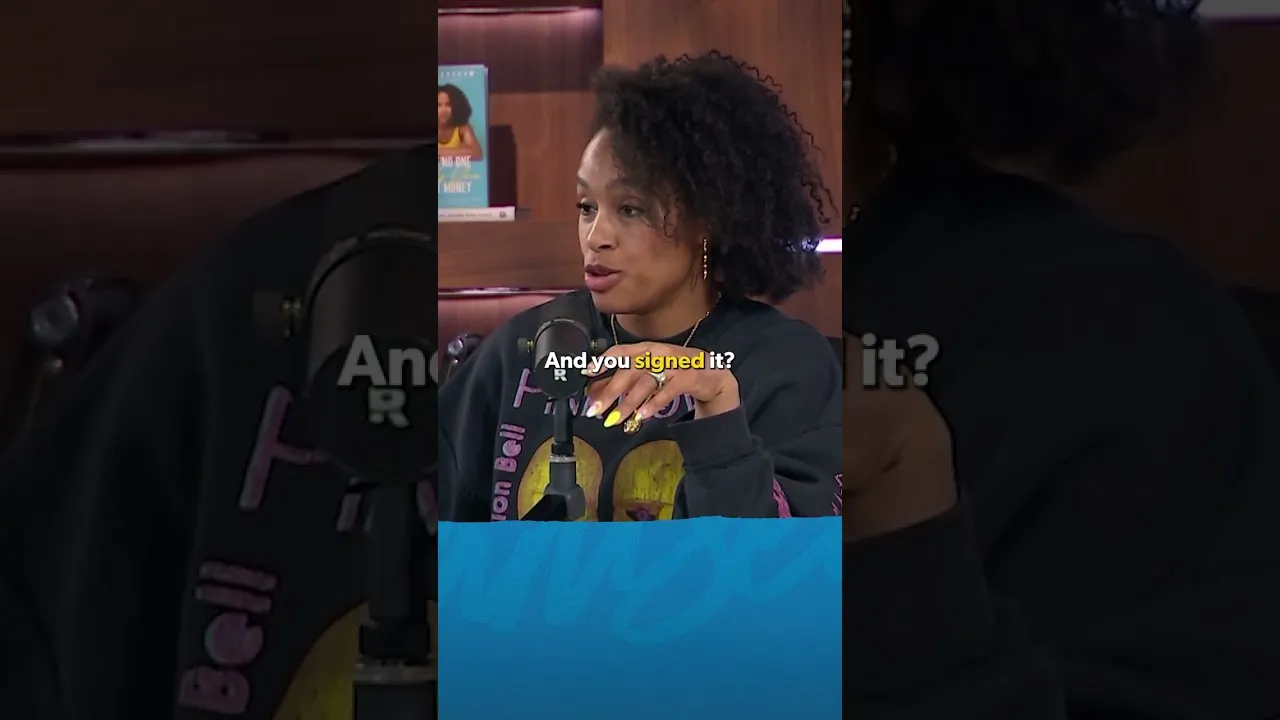

A Lawyer’s Promissory Note

Adding a layer of legal complexity, the daughter revealed that her father, a lawyer, had her sign a promissory note before the funds were disbursed for her education. This note stipulated that she would repay all sums paid to her for her secondary education. At the time of signing, she perceived the note more as a symbolic gesture of her obligation rather than a strict financial contract for the full account balance, including growth.

Upon reviewing the note as an adult, the fine print indicates a commitment to repay all sums paid to her. The daughter’s surprise and dismay underscore a potential disconnect between the initial understanding of the agreement and its current interpretation by the parents.

The Disconnect in Understanding

The core of the dispute appears to lie in the differing interpretations of the 529 plan’s balance and the promissory note. The parents seem to be requesting repayment of the account’s final valuation, which includes investment gains. This perspective suggests a belief that the entire sum, irrespective of its origin (contributions vs. growth), is a debt owed by the daughter. Conversely, the daughter’s understanding, as expressed, was likely that she would be responsible for the principal amounts used, or perhaps a more modest repayment reflecting her direct benefit.

Market Impact and Investor Considerations

While this situation is highly personal, it touches upon broader themes relevant to investors and families navigating educational savings.

- Understanding Investment Growth: For families utilizing 529 plans or other investment vehicles for education, it’s crucial to have clear discussions about expectations regarding investment growth. The growth is a feature of the investment, not an additional loan amount.

- Clarity in Agreements: When financial arrangements are made, especially between family members, clear, written agreements are paramount. A legally binding document like a promissory note can have significant implications, and all parties should fully understand its terms and consequences.

- Financial Literacy and Communication: This case highlights the importance of financial literacy for all involved. Open and honest communication about financial expectations, responsibilities, and potential outcomes can prevent misunderstandings and preserve relationships.

Long-Term Implications

The immediate implication for the daughter is a substantial financial obligation that could impact her personal finances for years to come. The long-term implications extend to the family dynamic, potentially causing irreparable damage to the relationship between the parents and their daughter. Legally, the enforceability of the promissory note and the parents’ claim will depend on the specific wording and jurisdiction.

“Let him take you to court. I think this would be a hilarious way to end the relationship with his daughter. What a way to go.”

This narrative serves as a cautionary tale, emphasizing the need for transparent financial planning and clear communication when significant sums of money are involved, especially within family contexts. Investors and parents alike should ensure that educational savings plans are managed with clear intentions and agreements to avoid such potentially contentious situations.

Source: Her Dad Made Her Sign a Ridiculous Contract (YouTube)