Homeownership Becomes Unaffordable for Average American

Buying a home in America feels increasingly out of reach for many. A recent analysis reveals a significant gap between the cost of a median-priced home and the income of the typical American household. This widening disparity makes the dream of homeownership a tough challenge.

Understanding the Numbers: What Salary Buys a Home?

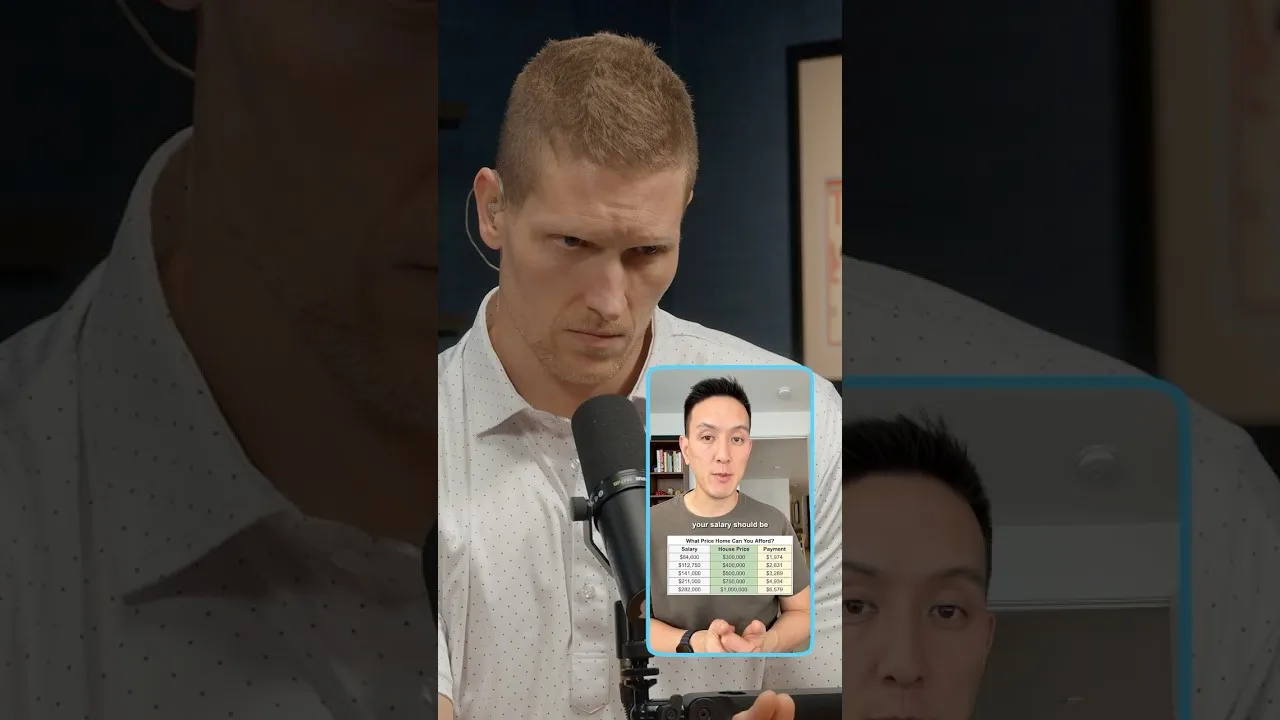

To illustrate the affordability crisis, one calculation used a 6% interest rate on a 30-year mortgage. This allowed for an estimate of monthly mortgage payments for different home prices. For example, a $400,000 home would require a monthly mortgage payment of $2,631. To comfortably afford this payment, assuming a 28% rule for housing expenses, a salary of $112,750 per year is suggested.

These figures include monthly property taxes and insurance. The calculation also assumed a substantial 20% down payment. This upfront cost adds another significant hurdle for potential buyers.

The Stark Reality: Median Income vs. Median Home Price

The median price of a home in America recently stood at $410,000. However, the median household income is much lower, around $84,000 per year. This data point is critical: the average household income is no longer sufficient to purchase the average-priced home in the country.

This means that for many families, the financial requirements for buying a home have become nearly impossible to meet. The gap highlights a major shift in the housing market that impacts millions of Americans.

Alternative Affordability Rules for First-Time Buyers

While the 28% rule is a common guideline, some experts suggest a more flexible approach, especially for first-time homebuyers. The 3/25 rule is one such guideline. It suggests aiming for a total housing expense that does not exceed 25% of your gross monthly income.

Crucially, this rule acknowledges that first-time buyers may not have a 20% down payment saved. It suggests that putting down as little as 3% to 5% can be acceptable for a first home. This can significantly lower the initial barrier to entry.

Long-Term Commitment: Staying Put

A key part of making homeownership work, especially with a lower down payment, is the intention to stay in the home for a considerable period. Experts recommend that buyers should plan to live in their new home for at least 5 to 7 years. This timeframe helps to build equity and allows time for the property value to potentially increase.

Staying longer in a home can help offset the costs associated with buying and selling. It also allows homeowners to benefit from their investment over time. This long-term perspective is vital for successful homeownership.

Market Impact

The current housing market dynamics, with high prices and rising interest rates, are creating a challenging environment. The gap between median income and median home prices suggests that demand for entry-level homes may remain strong, but affordability will be the primary constraint. This could lead to increased demand for rental properties and potentially slower home sales volume in the short term.

For the broader market, this trend could influence consumer spending patterns, as a larger portion of income is potentially tied up in housing costs or unattainable housing dreams. It also raises questions about housing supply and the need for more affordable housing options.

What Investors Should Know

Investors looking at the real estate sector should be aware of these affordability challenges. While the median home price remains high, the ability of the average buyer to purchase is limited. This could mean that properties at the lower end of the market, or those requiring renovation, might see sustained interest from buyers who can find ways to manage the costs.

The emphasis on longer-term residency for buyers using lower down payments suggests that the market for starter homes might be more stable, as owners are less likely to sell quickly. Understanding these buyer behaviors is key to assessing investment opportunities in the current climate.

Source: This Is Why Buying a Home Feels Impossible (YouTube)