Retirement Savings: Less May Be More

Many people believe a million-dollar nest egg is required for a comfortable retirement. However, new analysis suggests that significantly smaller portfolios could provide a steady income stream. This challenges the common belief that a massive savings amount is essential for financial freedom in later life.

Understanding Retirement Income Streams

The key to a comfortable retirement often lies in combining different income sources. For retirees, these typically include Social Security benefits and withdrawals from their investment portfolios. Understanding how these two streams work together is crucial for planning.

Social Security Benefits

Social Security provides a vital income base for many retirees. The average monthly benefit, based on current data, is around $2,071 per person. For a couple retiring at age 67, this could mean a combined monthly income of approximately $4,142 from Social Security alone.

Portfolio Withdrawal Rates

How much can you safely take out of your savings each year? The traditional “4% rule” suggested withdrawing 4% of your portfolio annually. However, recent analysis by the founder of the 4% rule has revised this figure upwards to 4.7%. This means you might be able to withdraw a slightly larger amount each year while still preserving your capital for longer.

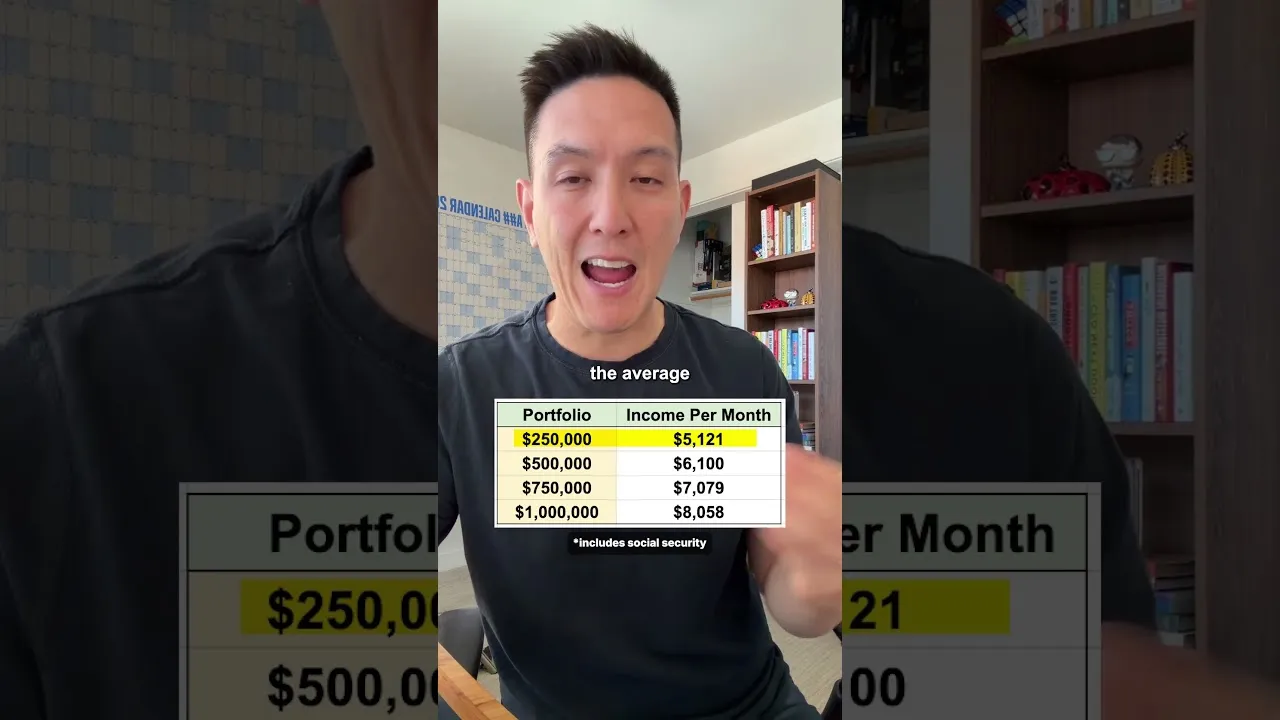

Income Projections for Different Portfolio Sizes

Let’s look at how different savings amounts could translate into monthly income, assuming a couple, both receiving the average Social Security benefit, and using the 4.7% withdrawal rate:

- $250,000 Portfolio: This could yield approximately $5,121 per month. This income comes from about $1,170 from the portfolio (4.7% of $250,000 annually, divided by 12) plus roughly $3,951 from Social Security for the couple.

- $500,000 Portfolio: This size portfolio could generate around $6,100 per month. This includes about $1,958 from the portfolio (4.7% of $500,000 annually, divided by 12) plus the Social Security income. This amounts to an annual income of about $73,000.

- $750,000 Portfolio: With this amount, retirees could expect a monthly income of roughly $7,000. This includes about $2,938 from the portfolio plus Social Security.

- $1,000,000 Portfolio: A full million-dollar portfolio could provide about $8,000 per month. This consists of approximately $3,917 from the portfolio plus Social Security.

Retiree Spending Habits

Many retirees find they spend less than they anticipated. Often, major expenses like mortgages are paid off. The primary costs then become healthcare, travel, and discretionary spending like dining out. This reduced spending can make smaller portfolio amounts more viable.

Market Impact

The idea that less capital may be needed for retirement could influence how individuals approach savings and investment strategies. It may encourage some to consider earlier retirement if their savings align with these income projections. Conversely, it could also lead to a re-evaluation of spending habits during working years.

What Investors Should Know

This analysis suggests that a well-planned retirement income strategy, combining Social Security with a revised withdrawal rate, can stretch savings further. Investors might feel more confident about their retirement readiness with smaller, yet adequate, portfolio balances. However, it’s important to remember that these are projections based on averages and a specific withdrawal rate. Individual circumstances, market performance, and inflation can significantly impact actual retirement income.

“Most retirees will spend a lot less money than they think. They also have their homes paid off. And really, all they’re paying for is healthcare and travel and perhaps eating out.”

The revised 4.7% withdrawal rate, compared to the traditional 4%, allows for a slightly higher income draw. This can make a significant difference, especially for those with smaller portfolios. For instance, a $250,000 portfolio at 4.7% withdrawal provides over $5,000 monthly, a figure that could support a modest lifestyle for many couples, especially when supplemented by Social Security.

Long-Term Implications

For those nearing retirement, this information could provide a more realistic outlook on their financial preparedness. It might alleviate some anxiety about needing to accumulate extremely large sums. For younger investors, it reinforces the importance of consistent saving and smart investment, but perhaps with less pressure to reach sky-high targets. The key takeaway is that retirement planning is personal and depends heavily on individual spending needs and income sources.

Source: Is $250k, $500k, $750k, and $1M enough to retire on? I answer it. (YouTube)