Smart Money Moves: Where to Put Cash After Each Paycheck

Every time you receive a paycheck, deciding where to allocate your money is crucial for financial health. A clear, step-by-step approach can help build savings, manage debt, and grow wealth. This strategy prioritizes essential payments and builds a solid financial foundation before moving to investment opportunities.

Step 1: Minimum Debt Payments

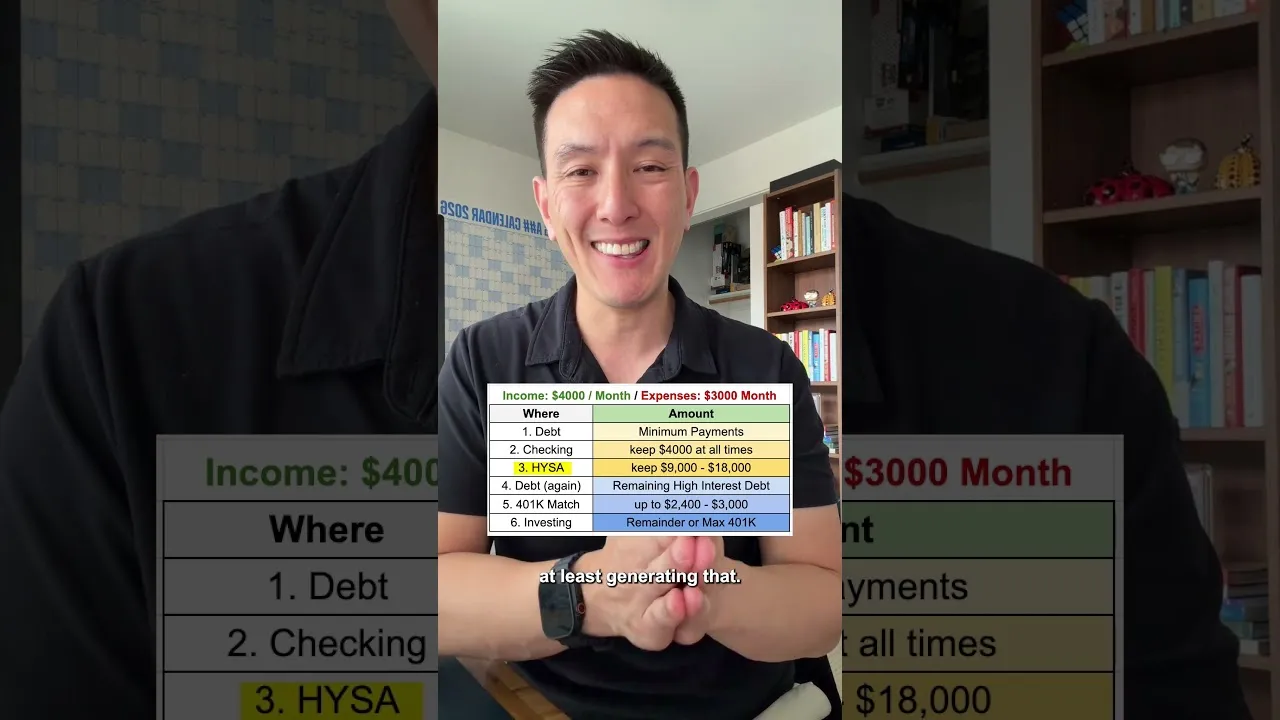

The very first financial action should be making at least the minimum payments on any outstanding debts. This is vital because timely payments are a major factor in maintaining a good credit score. A strong credit score can lead to better interest rates on future loans, like mortgages or car payments.

Step 2: Bolster Your Checking Account

Next, ensure your checking account has a comfortable buffer. For instance, if your monthly expenses total $3,000, aiming to keep at least $4,000 in your checking account provides a safety net. This buffer helps prevent overdraft fees and offers peace of mind, ensuring bills are covered even if there’s a slight delay in income or an unexpected small expense.

Step 3: Build an Emergency Fund

A critical step is establishing an emergency fund. The goal is to save enough to cover three to six months of living expenses. This money should be held in a high-yield savings account, which currently offers interest rates around 3% to 3.5%. Having this fund readily available is essential for unexpected events like job loss or medical emergencies, preventing you from going into debt.

Step 4: Tackle High-Interest Debt

Once your emergency fund is on track, focus on paying down high-interest debt. Any debt with an interest rate above 10% is generally considered high-interest. Aggressively paying this down saves you a significant amount of money on interest charges over time and frees up cash flow faster.

Step 5: Capture Your 401(k) Match

A highly beneficial move is to contribute enough to your employer-sponsored 401(k) plan to get the full company match. This is essentially free money and offers a very high immediate return on your investment. For example, if your employer matches 50% of your contributions up to 6% of your salary, contributing that 6% guarantees you an instant 50% return on that portion of your savings.

Step 6: Invest for the Future

After covering the previous steps, any remaining money can be invested. Options include contributing to a Roth IRA, maximizing your 401(k) contributions beyond the match, or investing in a standard taxable brokerage account. These investments can help grow your wealth over the long term through compounding returns.

The Waterfall Approach

It’s recommended to follow these steps in a specific order, often called a waterfall. You start with step one and move sequentially through step six. This ensures that your most pressing financial needs and immediate gains are addressed before moving on to longer-term investment goals.

Market Impact and Investor Considerations

This structured approach to personal finance has several implications for investors. Prioritizing debt repayment and building an emergency fund reduces financial risk. This allows individuals to invest more confidently and with a greater capacity for growth.

Capturing the 401(k) match is a guaranteed return that many investors overlook. It’s a foundational step in retirement planning. For those with high-interest debt, paying it down aggressively is often a better guaranteed return than many market investments. This is because the interest saved is a certain gain, unlike market performance which can fluctuate.

Finally, investing in tax-advantaged accounts like a Roth IRA or a 401(k) offers significant long-term benefits. These accounts allow your investments to grow tax-deferred or tax-free, enhancing your overall returns. For any remaining funds, a taxable brokerage account provides flexibility for various investment goals.

By consistently applying this waterfall method with each paycheck, individuals can systematically improve their financial standing, reduce debt burdens, and build a strong foundation for long-term wealth creation.

Source: 6 Places Your Money Should Go Every Time You Get Paid (YouTube)