Home Prices Soar, Leaving Many Americans Priced Out in 2026

Buying a home in 2026 is becoming a far-off dream for many Americans. With mortgage rates at 6% and the median home price hovering around $400,000, the math of homeownership is tougher than ever. Running the numbers reveals that a large portion of the population struggles to afford even a moderately priced house, let alone a million-dollar property.

Understanding Home Affordability Rules

Traditionally, banks use the 28/36 rule to determine mortgage eligibility. This rule suggests that your monthly mortgage payment, including taxes and insurance, shouldn’t exceed 28% of your gross monthly income. Additionally, all your monthly debt payments, including your mortgage, should not be more than 36% of your gross income.

For example, if you earn $100,000 a year, your gross monthly income is about $8,333. Under the 28% rule, your mortgage payment (including taxes and insurance) should be around $2,333 per month. This rule helps banks assess risk, but it doesn’t account for crucial homeownership costs like maintenance, utilities, or potential homeowners association (HOA) fees.

A more realistic approach, according to some analysts, is to aim for total housing costs (mortgage, taxes, insurance, HOA fees) to be under 30% of your net income – the money you actually take home after taxes. Gross income can be misleading because it doesn’t reflect the reality of your take-home pay, especially after retirement contributions like 401(k)s.

The Cost of a $250,000 Home

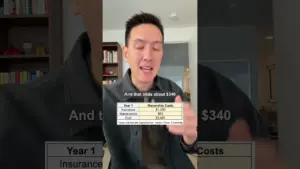

Let’s look at a $250,000 house. Assuming a 20% down payment ($50,000) and a 6% mortgage rate on a 30-year loan, the principal and interest payment would be about $1,199 per month. Adding property taxes and insurance brings the total to roughly $1,500 to $1,700 per month. To comfortably afford this using the 30% net income rule, assuming a 75% take-home pay rate, you’d need a gross annual salary of about $85,000. The bank might approve you with a lower income based on its rules, but living comfortably requires more.

The $500,000 Home: A Significant Leap

A $500,000 home, which is about $100,000 above the median U.S. home price, requires a substantial down payment of $100,000 (20%). The loan amount would be $400,000. The principal and interest payment alone would be around $2,398 per month. With taxes and insurance, the total monthly cost could reach $2,800 to $3,000. To stay within the 30% net income guideline, a household would need a net monthly income of about $10,000, translating to a gross annual income of approximately $160,000. This often means a dual-income household, where both earners make around $80,000 annually.

The Million-Dollar Mark: Out of Reach for Most

For a $1 million home, the down payment jumps to $200,000 (20%), leaving $800,000 to finance. The monthly principal and interest payment would be nearly $4,800. Including taxes and insurance, the total monthly housing cost could easily hit $5,800 to $6,300. To afford this comfortably, a household would need a net monthly income of about $20,000, requiring a gross annual income of roughly $320,000. This places affordability for a million-dollar home within the top 5% of U.S. households.

The $2 Million Home: An Elite Tier

Purchasing a $2 million home is even more exclusive. A 20% down payment requires $400,000 in cash. The loan amount of $1.6 million would result in principal and interest payments of almost $9,600 per month. With taxes, insurance, and potentially higher maintenance costs, the total monthly expense could reach $12,000 to $13,000. This level of affordability requires a net monthly income of around $40,000, translating to a gross annual income of approximately $700,000. Only about 2% of American households can manage this.

Market Impact: The Growing Affordability Gap

The stark reality is that the gap between what Americans earn and the cost of housing is widening. This discrepancy is a major driver of the current housing crisis. While mortgage rules provide a baseline for qualification, they don’t guarantee true affordability or financial well-being.

What Investors Should Know

For potential homebuyers, the key takeaway is to conduct a thorough personal budget analysis. Relying solely on bank-approved numbers or outdated rules of thumb can lead to financial strain. Understanding your net income and factoring in all potential homeownership costs is crucial for making a sound decision. The data suggests that for many, especially in high-cost areas, achieving homeownership at higher price points will require significant financial resources, dual incomes, or substantial financial assistance.

The increasing difficulty in affording homes at various price points has broader implications for the economy, potentially impacting consumer spending, migration patterns, and demand for housing in different regions.

Source: Who Can Afford a $250K, $500K, $1M, and $2M House in 2026? (YouTube)