Millions Face Financial Strain, Experts Offer Debt-Free Path

Many households are struggling with overwhelming debt, facing difficult choices about their financial future. For those looking to avoid bankruptcy, a path to becoming debt-free exists, though it requires significant commitment and sacrifice. Experts suggest that with intense focus and strategic planning, families can eliminate substantial debt in just a few years.

The Math of Debt Freedom

Consider a scenario where a household brings home $50,000 annually after taxes. If their mortgage payment is covered, they might have around $11,000 left each month. The key to rapid debt reduction lies in aggressively allocating funds towards paying down what is owed. For instance, dedicating $6,000 per month to debt repayment could clear a significant amount.

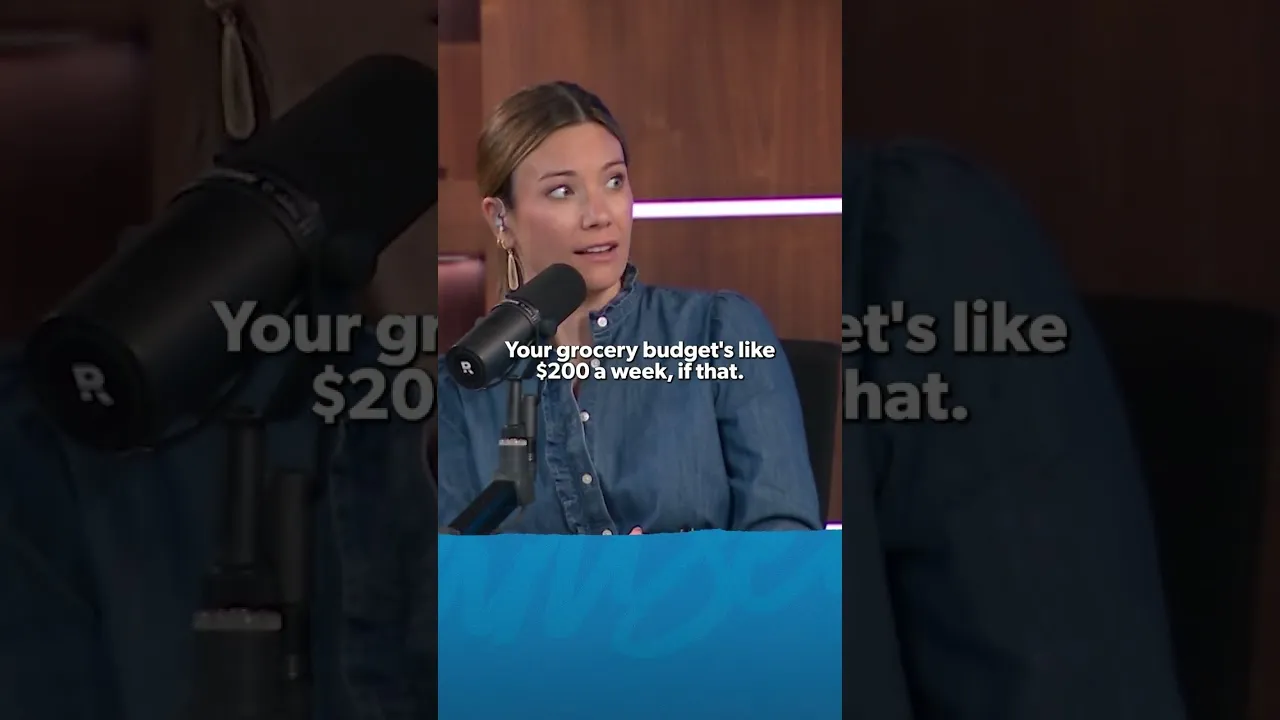

This level of commitment means drastically cutting living expenses. A suggested grocery budget of around $200 per week illustrates the necessary lifestyle changes. It implies a period where almost all available income is channeled into debt elimination, with little left for discretionary spending. This intense focus is not a long-term solution but a temporary, demanding strategy.

Aggressive Repayment Timeline

By committing to paying an extra $6,000 monthly, a substantial debt load could be cleared in under three years. This timeline is based on strict budgeting and prioritizing debt repayment above all else. The experts emphasize that this is a period of intense effort, often described as “grinding it out.” This phase could realistically last between three to three and a half years.

Beyond Income Allocation

The repayment strategy doesn’t solely rely on reallocating existing income. Additional measures can accelerate the process. Selling unused items or taking on extra work can provide lump sums to further reduce the principal owed. These actions supplement the aggressive monthly payments, shortening the overall debt-free timeline.

The Reality of the Grind

Achieving debt freedom without bankruptcy requires a serious commitment. It means making significant lifestyle adjustments for a sustained period. This could involve cutting back on entertainment, dining out, and other non-essential expenses. The focus shifts entirely to financial recovery, making it a temporary but challenging phase.

Market Impact

While this advice focuses on individual household finances, widespread debt reduction could eventually impact consumer spending patterns. A population less burdened by debt may increase discretionary spending over the long term. However, the short-term effect of such aggressive repayment plans is reduced consumer activity as individuals prioritize saving and debt elimination.

What Investors Should Know

For investors, understanding these personal finance trends can offer insights into consumer behavior. Sectors reliant on discretionary spending might see slower growth during periods of widespread debt reduction efforts. Conversely, companies focused on essential goods and services may remain more stable. The long-term potential for increased consumer spending after debt is cleared presents opportunities for growth-oriented investors.

Short-Term Implications

In the immediate future, households aggressively paying down debt will likely reduce their spending on non-essentials. This could affect retail, entertainment, and travel sectors. Banks and lenders might see slower growth in new loan origination as consumers focus on paying off existing debts.

Long-Term Implications

Once significant debt is eliminated, individuals often have more disposable income. This can lead to increased spending on larger purchases, investments, and other financial goals. Over the long haul, a healthier consumer balance sheet can boost economic growth and create opportunities across various market sectors. This shift towards financial stability can create a more robust consumer base.

Context and Caution

It’s important to remember that this strategy is demanding. Not everyone can sustain such a high level of sacrifice for several years. Financial advisors often recommend personalized plans that balance debt repayment with quality of life. The goal is sustainable financial health, not just rapid debt elimination at any cost.

Source: How Do We Get Out of Our Financial Mess Without Bankruptcy? (YouTube)