Young Couple Grapples with Over $20,000 in High-Interest Debt

A 20-year-old couple is facing a significant financial challenge with over $20,000 in debt, much of it carrying extremely high interest rates. The situation highlights the dangers of accumulating debt without careful consideration, especially for young individuals starting their financial journey.

The husband, Oscar, detailed his debt load, which includes $2,000 on a credit card at 17% interest, $3,500 on another card at a staggering 30% interest rate, and $1,200 on a third card at 0% interest. He also has $2,800 in debt currently in collections.

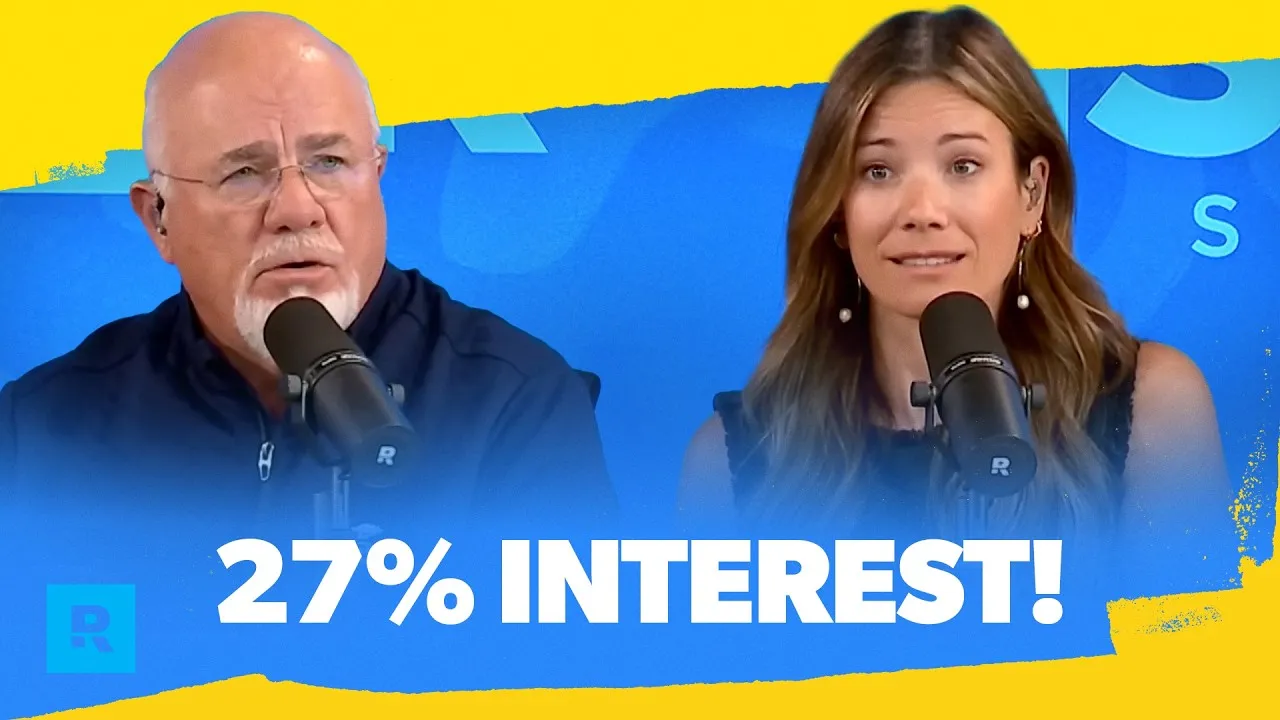

Adding to this burden is his wife’s car loan, which has a $10,000 balance with an alarming 27% interest rate. The couple has already paid $8,000 towards this car loan over three years, which originally had a $13,000 balance.

Financial Strain on Young Family

The couple’s financial picture is further complicated by their income and living situation. Oscar earns $2,600 per month after taxes from his job managing a Chipotle.

His wife does not work outside the home as she cares for their one child. They are currently living with his wife’s parents, a situation stemming from a previous apartment where rent was paid using credit cards after Oscar lost a job he had lined up.

“You’re 20 years old with a baby. You live with her parents.

You make $2,600 a month and you apparently don’t read anything before you sign debt because you’ve got some of the worst debt products on the planet,” commented a financial analyst observing the situation. “Everything you had was north of 20%.” This indicates a pattern of taking on debt without fully understanding the terms and consequences.

Available Cash vs. Debt Obligations

Despite the debt, the couple has managed to save $8,800 in cash. Oscar expressed a desire to pay off his wife’s car immediately, noting that it could be paid off within a month.

He believes this would free up the $500 monthly car payment to be directed towards other debts and savings. This strategy, however, is being weighed against the possibility of using the cash to tackle other, smaller debts first.

The total debt, excluding the car loan, amounts to approximately $9,500 ($2,000 + $3,500 + $1,200 + $2,800). The car loan adds another $10,000, bringing the total debt to around $19,500. With $8,800 in cash, the couple is within reach of becoming debt-free, excluding the car, by using a significant portion of their savings.

Recommendations for Debt Reduction

Financial experts suggest a strategic approach to tackle this debt. One recommendation is to use the $8,800 in savings to pay off the smaller debts first, starting with the $1,200 credit card, then the $2,000 credit card, followed by the $2,800 in collections, and finally the $3,500 credit card. This would clear all credit card and collection debts, leaving only the car loan.

After clearing these debts, the couple would have a small emergency fund remaining from their $8,800 savings. The next critical step would be to aggressively pay down the $10,000 car loan. Experts advise generating additional income to accelerate this payoff.

Oscar’s upcoming promotion, which will increase his hours and income, is a positive step. However, even with the promotion, significant additional income generation is needed.

Boosting Income is Key

To accelerate debt payoff and improve their financial standing, the couple needs to significantly increase their monthly income. The advice given was to aim for an extra $2,000 per month. This could be achieved through multiple part-time jobs or side hustles, such as delivery services or other available work, until Oscar’s career path leads to higher earnings.

“You need two more part-time jobs,” was the direct advice. “You need to pile up some money so you can get out of your mother-in-law’s house.” The urgency is tied to their current living situation and the high cost of their existing debt.

Long-Term Financial Planning

Beyond immediate debt reduction, the couple is encouraged to focus on long-term financial planning and career development. At 20 and 21 years old, they have a long runway to build wealth, but this requires a fundamental shift in how they approach debt and income.

A crucial step is to stop acquiring new debt, especially high-interest debt. Experts strongly advise cutting up credit cards and committing to a strict budget using tools like the Every Dollar app. Future financial decisions should be guided by a clear understanding of income, expenses, and the long-term consequences of borrowing.

What Investors Should Know

This situation highlights the pervasive issue of high-interest debt, particularly among younger demographics. The 27% interest rate on the car loan is exceptionally high and indicative of predatory lending or poor financial choices. Such high rates significantly inflate the cost of borrowing, making it much harder to get ahead financially.

For investors, this is a cautionary tale about the impact of consumer debt on personal financial health and economic mobility. High debt burdens can stifle savings, prevent investment, and create prolonged financial stress. The couple’s reliance on credit for basic needs like rent during a period of unemployment also highlights financial vulnerability.

The advice to seek career counseling and books like Ken Coleman’s “Find the Work You’re Wired to Do” points to the importance of increasing earning potential as a primary strategy for long-term financial success. Focusing on career growth that leads to higher income is often more effective than solely focusing on cutting expenses, especially when income is currently very low.

Future Outlook

Oscar’s upcoming promotion and the couple’s willingness to consider additional jobs are positive indicators. If they can successfully implement a strict budget, cut up their credit cards, and aggressively pay down their debt, they can become debt-free relatively quickly. The key will be sustained effort and a commitment to avoiding future high-interest debt.

The couple plans to cut up their credit cards and use debit cards with a strict budget. They are also exploring resources to help Oscar find fulfilling work that can increase his long-term income potential. The immediate goal is to eliminate their current debt load and establish a solid financial foundation for their young family.

The couple is encouraged to schedule a service at Christian Brothers Automotive for their vehicles and use the promo code RAMSEY for a discount, as recommended by their financial advisor.

Source: "You Signed Up For Some Of The Worst Debt Possible" (YouTube)