Savings Rate Dominates Returns for Retirement Success

Two individuals with identical salaries, job titles, and career timelines can experience vastly different financial outcomes by retirement. One might achieve complete financial independence by age 55, while the other could still be working at 75, not by choice but by necessity.

This divergence isn’t due to income levels, investment performance, luck, or market timing. Instead, it hinges on a single, consistent decision made month after month: their savings rate.

The crucial decision determining one’s financial future is the savings rate, the percentage of income saved and invested regularly. This factor holds more weight than nearly any other financial choice.

Early in a career, earning income drives wealth building. However, as savings and investments grow, compound growth allows saved money to work harder, effectively creating an “army of dollar bills” that handles more of the heavy lifting.

The savings rate dictates the size of this financial army. It directly impacts not only the total wealth accumulated by retirement but also the timeline to achieve financial independence.

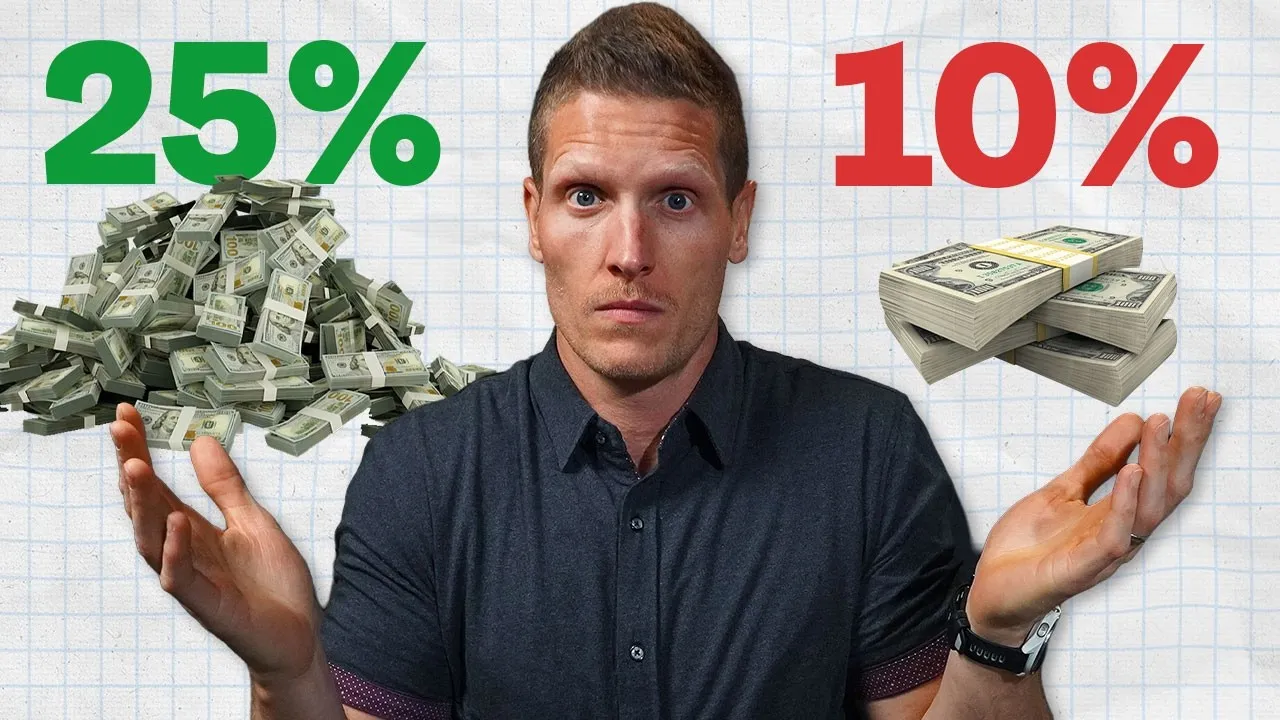

A higher savings rate can accelerate the journey to early retirement, even with less impressive investment returns. This was illustrated by comparing two hypothetical individuals, Manny the Mutant and Average Allen, both earning $100,000 annually.

Average Allen saved 10% of his income and achieved a strong 10% average annual return. Over 30 years, he accumulated approximately $1.8 million. In contrast, Manny the Mutant saved a higher 25% of his income but earned a more modest 6% average annual return.

Despite the lower returns, Manny’s higher savings rate allowed him to surpass $2 million in savings over the same 30-year period. Crucially, Manny reached the $1 million milestone four years earlier than Allen, demonstrating that a higher savings rate can lead to earlier financial freedom and greater overall wealth.

This comparison highlights a fundamental principle: you can compensate for lower investment returns with consistent, higher savings, but you cannot overcome a low savings rate with exceptional returns. No investment strategy, regardless of its sophistication, can replace the foundational need to save a sufficient amount.

Without this base, the power of compounding cannot be fully realized. A low savings rate not only diminishes potential wealth but also extends the working years needed to reach retirement.

Every significant financial decision, from purchasing a home or car to planning vacations, ultimately affects one’s retirement timeline. These choices often involve prioritizing immediate comfort or pleasure over future financial freedom. This appears to be a common trend among Americans.

Data from the Federal Reserve indicates that the median retirement account assets for individuals nearing retirement (ages 55-64) is approximately $185,000. Applying the standard 4% withdrawal rule, this amount would only generate about $7,400 in annual income during retirement.

Creating Financial Margin is Key

A major obstacle preventing many from increasing their savings rate is a lack of “financial margin.” This margin is the gap between income earned and expenses paid. Without this buffer, there are no extra dollars available to save or invest. According to Market Watch, 57% of Americans report living paycheck to paycheck, indicating minimal funds left after covering essential bills.

To create this essential financial margin, two primary actions can be taken: spending less or earning more. Reducing expenses is often a practical starting point, as “lifestyle creep” can hinder savings. This occurs when income increases, leading to a corresponding rise in spending habits, keeping the savings rate stagnant.

Automating investments, such as setting up automatic contributions to 401(k)s and Roth IRAs, is an effective strategy. By having funds transferred before they are seen in a checking account, individuals are less likely to spend the money.

Another method to manage expenses is the “60/40 rule.” When receiving a raise or bonus, allocating 60% towards savings and investments while dedicating 40% to lifestyle upgrades offers a balanced approach. This strategy allows for enjoying the rewards of hard work while still making progress toward financial objectives. The consistent percentage of income set aside month after month, year after year, is what truly differentiates those who retire comfortably in their mid-50s from those still working in their mid-70s.

Recommended Savings Target and Next Steps

A recommended benchmark for savings is 25% of gross income. This target generally places individuals on a path toward substantial financial independence.

For example, saving 25% for retirement by age 30, assuming a 6% annual return, could potentially replace nearly 120% of pre-retirement income by age 65, effectively providing a raise in retirement. However, the ideal savings rate varies based on individual factors like age, lifestyle, goals, and current financial standing.

Creating this margin is crucial for building wealth. For those struggling to reach a 25% savings rate, strategies like automating investments and the 60/40 rule for raises can help.

Understanding how to best utilize savings accounts and investment vehicles in the correct order is also vital for maximizing growth. The “Financial Order of Operations” provides a step-by-step guide for managing financial resources effectively.

The core message is that consistent saving is the most powerful driver of long-term financial success. Even with moderate investment returns, a high savings rate can secure a comfortable retirement. The decision to prioritize saving today directly shapes financial freedom tomorrow.

Source: This One Decision Determines Your Financial Future (YouTube)