Average Car Payment Hits $767: Are You Buying a Car or a Trap?

The average monthly payment for a new car in America has climbed to a staggering $767. This figure, according to recent data from Experian, represents a significant financial commitment that many drivers don’t fully consider, especially concerning its long-term impact on their wealth-building goals.

Many consumers focus solely on whether a monthly payment fits their immediate budget, often overlooking crucial financial rules. This approach can lead to being financially constrained for years, hindering progress towards retirement and other financial aspirations. Understanding how much car you can truly afford based on your income is essential for making sound financial decisions.

Key Car Buying Rules for Financial Health

Two primary guidelines help determine if a car purchase is wise or a potential financial pitfall: the 2410 rule and the more conservative 238 rule.

The 2410 Rule

This widely recommended guideline suggests several key principles for car buying:

- Put down at least 20% of the vehicle’s price.

- Finance the car for no more than four years (48 months).

- Keep total monthly transportation costs (including payment, insurance, gas, and registration) under 10% of your gross monthly income.

The 238 Rule

A more conservative approach, often favored by financial experts, is the 238 rule:

- Maintain the 20% down payment.

- Shorten the loan term to a maximum of three years (36 months).

- Limit total monthly transportation costs to 8% of your gross monthly income.

The logic behind the 238 rule is simple: if you cannot pay off a depreciating asset like a car within three years, you are likely buying more vehicle than you can comfortably afford. The choice between these rules reflects an individual’s commitment to building wealth versus projecting an image of financial success.

Understanding the True Cost of Car Ownership

A common mistake is treating the monthly car payment as the sole car expense. In reality, the total cost of ownership is much higher and includes several components that dealers often downplay:

- Car Payment: The amount financed over the loan term.

- Insurance: Costs can range from $100 to over $300 per month, depending on factors like age, location, and driving record.

- Gas: Fuel costs vary based on vehicle efficiency and driving habits.

- Maintenance and Repairs: Routine upkeep and unexpected fixes add to the expense.

- Depreciation: New cars lose about 20% of their value in the first year alone. Over five years, the average depreciation can be 45-50%. This means a $30,000 car could be worth only around $15,000-$16,000 after five years, representing a significant loss of value.

Salespeople often focus on the monthly payment because it’s the most attractive number, designed to encourage buyers to stop asking critical questions about the total financial commitment.

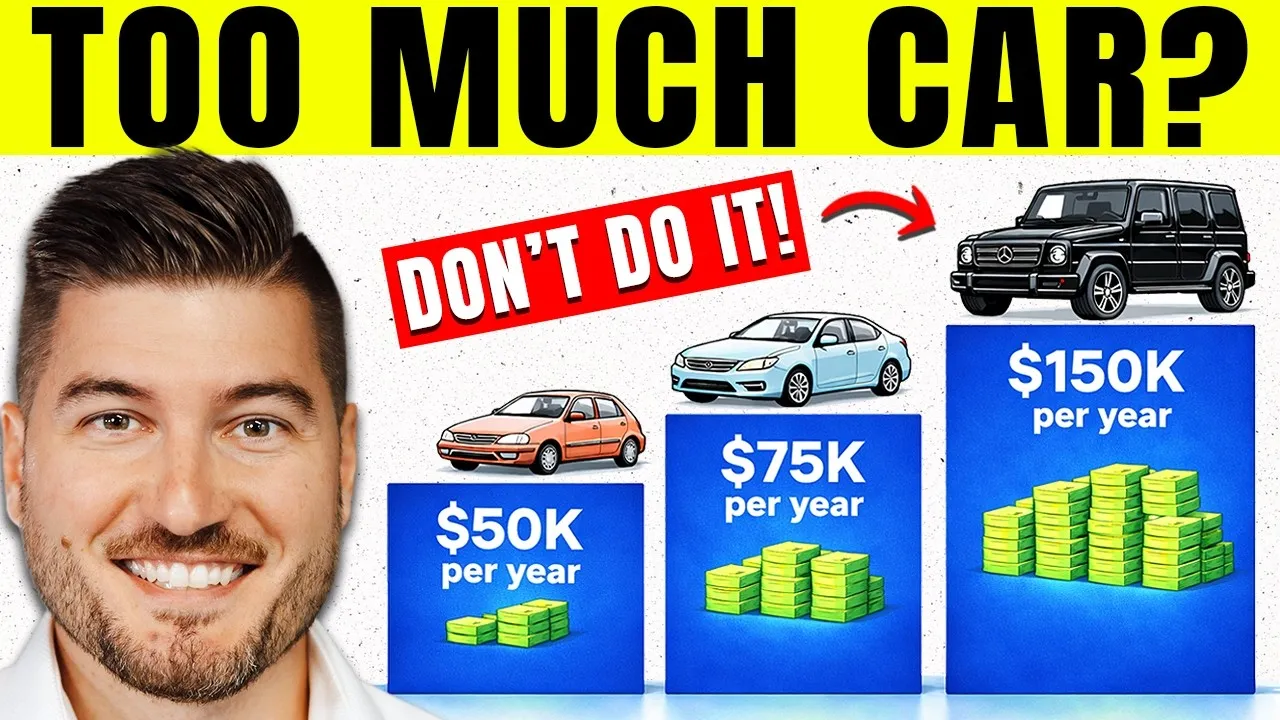

Affordability Based on Income Levels

Let’s break down car affordability using the 8% and 10% rules for different income brackets, assuming a generous monthly take-home pay after taxes.

$50,000 Annual Income

- Estimated Monthly Take-Home: ~$3,400

- 10% Transportation Budget: $340/month

- 8% Transportation Budget: $272/month

After accounting for insurance and gas (estimated at $150/month), this leaves $120-$190 for a car payment. With a 20% down payment, this budget supports a vehicle purchase in the $6,000-$8,000 range. This means prioritizing reliable transportation, such as a well-maintained used Honda Civic or Toyota Corolla, over a newer, more expensive model.

$75,000 Annual Income

- Estimated Monthly Take-Home: ~$5,100

- 10% Transportation Budget: $510/month

- 8% Transportation Budget: $408/month

With insurance and gas factored in, the car payment budget falls between $250-$350 per month. This range allows for a maximum purchase price of $11,000-$16,000, depending on which rule is applied.

$100,000 Annual Income

- Estimated Monthly Take-Home: ~$6,800

- 10% Transportation Budget: $680/month

- 8% Transportation Budget: $544/month

This income level offers a car budget supporting a purchase price of $22,000-$25,000. A common trap for six-figure earners is believing loan approval equates to affordability, leading them to purchase luxury vehicles. The key takeaway is that a paid-off $15,000 car and investing the difference will lead to greater wealth than financing a $60,000 truck.

$150,000 Annual Income

- Estimated Monthly Take-Home: ~$9,100

- 10% Transportation Budget: $910/month

- 8% Transportation Budget: $728/month

This income level supports a car payment between $500-$700 per month, allowing for a maximum purchase price of $30,000-$35,000. While this may seem conservative for the income, every dollar spent on a car payment is a dollar not invested. The opportunity cost of an expensive car at this level can be substantial over time.

The Cost of Extending Loan Terms

Dealers may offer to lower monthly payments by extending the loan term. For example, reducing a payment by $39 a month over six years could cost an extra $2,800 in interest. Extending a $20,000 car loan from four years to seven years at 5% interest can increase the total cost by over $1,600. Longer loan terms mean paying more for the same car and often coincide with increased repair costs as the vehicle ages.

The Finance Office Pitfalls

Dealership finance offices are significant profit centers. They often push add-ons like gap insurance, extended warranties, and paint protection. For buyers who follow the 20% down payment rule and purchase a reliable car within their budget, many of these extras are unnecessary. Gap insurance, for instance, is less critical if you are not underwater on your loan. Setting aside money for potential repairs can be a more financially sound strategy than paying for an extended warranty.

Market Impact and Investor Considerations

The trend of rising car payments and longer loan terms highlights a broader issue of consumer debt and financial strain. While the automotive sector sees strong sales, the underlying affordability crisis affects household budgets and limits discretionary spending. For investors, understanding consumer financial health is crucial when evaluating companies in the automotive, financial services, and retail sectors. The increasing cost of vehicles also impacts the used car market, though historically, purchasing older, well-maintained vehicles has been a more financially prudent choice for wealth building.

What Investors Should Know

- Consumer Debt Levels: Rising car payments contribute to overall consumer debt, which can impact economic growth and spending.

- Depreciation: The rapid depreciation of new vehicles underscores the importance of value retention when making large purchases.

- Interest Rates: Higher interest rates on car loans increase the total cost of ownership, further challenging affordability.

- Long-Term Wealth: The significant difference in long-term wealth between someone who buys affordably and invests the savings versus someone who overspends on a car is substantial. For example, saving an extra $200 per month on car payments and investing it could yield over $240,000 in 30 years at a 7% annual return.

Ultimately, making a car purchase should align with long-term financial goals. Prioritizing reliable transportation over luxury, adhering to strict budgeting rules, and understanding the total cost of ownership are critical steps toward building sustainable wealth.

Source: How Much Car Can You Actually Afford? (By Salary) (YouTube)