Credit Cards vs. Debit Cards: Weighing Rewards Against Risk

In the realm of everyday financial transactions, consumers often face a fundamental choice: the credit card or the debit card. While both plastic payment methods offer convenience, they diverge significantly in their impact on personal finances, rewards potential, and risk exposure. Understanding these differences is crucial for making informed spending decisions.

The Allure of Credit Card Rewards

Credit cards, at their core, allow users to borrow money from a financial institution to make purchases. This borrowed capital comes with the significant advantage of earning rewards. Many credit cards offer incentives such as cash back, travel miles, or points that can be redeemed for various goods and services. Essentially, by utilizing a credit card responsibly, consumers can get paid to spend.

Beyond rewards, credit cards provide an added layer of consumer protection. If a purchased item is faulty or fails to arrive, cardholders can dispute the charge with their credit card issuer and potentially reclaim their funds. This chargeback mechanism offers a strong recourse against fraudulent transactions or unsatisfactory goods.

The primary benefit of using a credit card lies in its ability to leverage the bank’s money first, allowing consumers to accrue rewards and benefit from enhanced purchase protection.

The Responsibility of Credit Card Use

However, the convenience and benefits of credit cards are contingent upon responsible usage. The critical caveat is the requirement to repay the borrowed funds on time. Failure to do so results in interest charges, which can quickly escalate the cost of purchases. Moreover, consistently missing payments can severely damage a consumer’s credit score, impacting their ability to secure future loans, mortgages, or even rent an apartment.

Debit Cards: Simplicity and Security of Own Funds

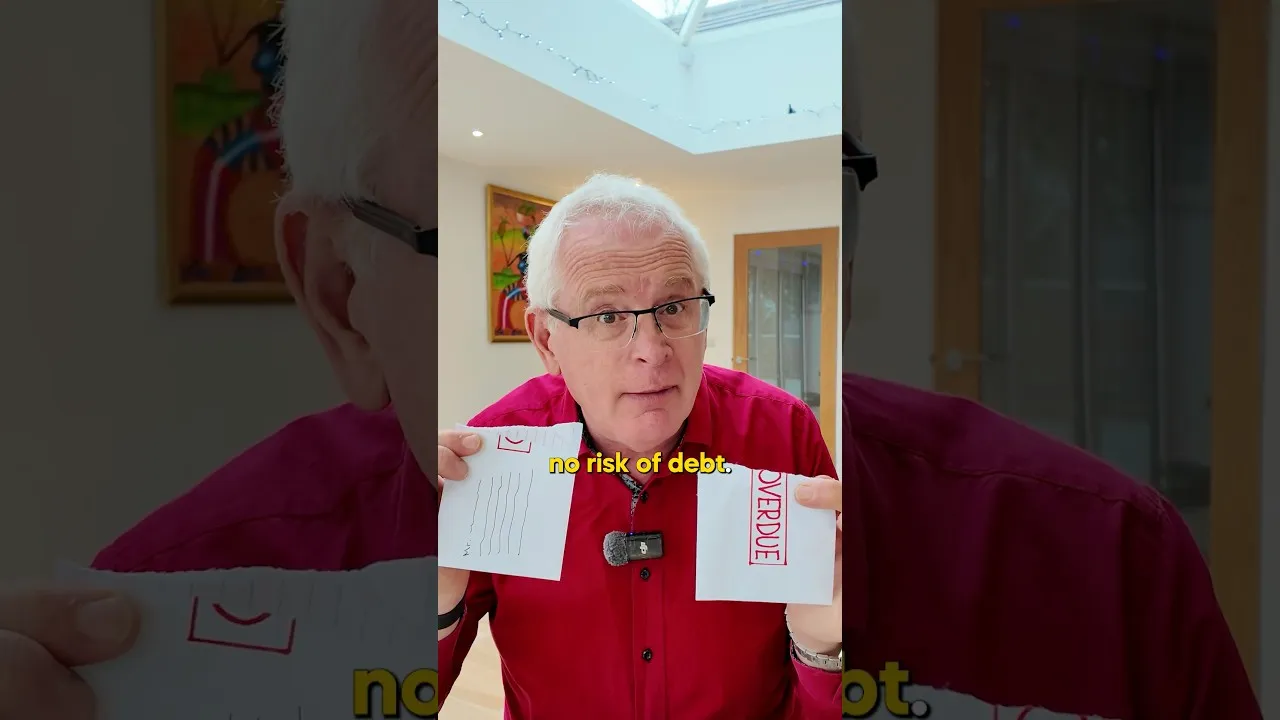

Debit cards, in contrast, are directly linked to a user’s bank account. When a purchase is made with a debit card, the funds are immediately deducted from the available balance in the associated checking or savings account. This direct transaction model offers a sense of security as it eliminates the risk of accumulating debt.

The primary appeal of a debit card is its straightforward nature: you spend the money you actually have. This prevents the possibility of overspending and falling into debt, which many consumers find reassuring. There is no interest to pay, and no credit score to damage through late payments, as no borrowing is involved.

The Trade-offs of Debit Card Usage

The simplicity and debt-free nature of debit cards come at a cost. Unlike credit cards, debit cards typically do not offer rewards programs. Consumers do not earn cash back or points for their spending. Furthermore, debit cards do not contribute to building or improving a credit history, which is a vital component for long-term financial health and access to credit.

The protection offered by debit cards is also generally less robust than that of credit cards. While some protections exist, they are often not as comprehensive as the chargeback rights afforded to credit card users. In cases of fraud or dispute, recovering funds from a debit card transaction can be more complex and time-consuming.

Market Impact and Investor Considerations

From a broader market perspective, the choice between credit and debit cards reflects a larger consumer behavior trend. The robust rewards programs offered by credit card companies are a significant driver of consumer spending and a key differentiator in the competitive financial services landscape. Issuers leverage these programs to attract and retain customers, influencing spending patterns and driving transaction volumes.

For investors, understanding the dynamics of the credit card industry involves looking at major issuers like Visa, Mastercard, American Express, and Discover. The profitability of these companies is directly tied to transaction volumes and the interest income generated from cardholder balances. Changes in consumer spending habits, interest rate environments, and regulatory policies can all impact these companies’ performance.

The growth of the credit card market, fueled by rewards and ease of use, contrasts with the more stable, albeit less dynamic, role of debit cards. While debit cards provide a steady stream of transaction fees for banks, credit cards offer higher potential for revenue through interest and fees, alongside the significant marketing advantage of rewards programs.

What Investors Should Know

The ongoing competition between credit and debit card usage highlights the consumer’s desire for both convenience and value. Credit cards, with their attractive rewards and purchase protections, continue to incentivize spending, albeit with the inherent risk of debt. Debit cards offer a safer, debt-free alternative, but forgo the benefits of rewards and credit building.

Investors in financial services companies should monitor consumer credit trends, interest rate sensitivity, and the effectiveness of rewards programs in driving cardholder engagement. The increasing adoption of digital payment methods further complicates this landscape, with both credit and debit functionalities being integrated into mobile wallets and other digital platforms.

Ultimately, the choice between a credit card and a debit card hinges on an individual’s financial discipline, spending habits, and goals. For those who can manage their balances responsibly and benefit from rewards, credit cards can be a powerful financial tool. For those prioritizing debt avoidance and simplicity, debit cards offer a secure way to manage daily expenses.

Source: Credit Card vs. Debit Card (YouTube)