Parents Demand Repayment of 529 Funds

A complex family financial dispute has emerged, centering on the use and expected repayment of funds from a 529 college savings plan. The situation highlights a critical imbalance of knowledge and power, raising questions about the intended purpose of these savings vehicles and the obligations of beneficiaries.

The Core of the Dispute

The central issue involves a situation where a parent, described as a lawyer, presented a document to their adult child, who then signed it without fully understanding its implications. The child had utilized funds from a 529 plan, a tax-advantaged savings account designed specifically for educational expenses. However, the parents are now reportedly expecting the child to repay these funds, framing it as a form of loan rather than a gift or an intended use of educational savings.

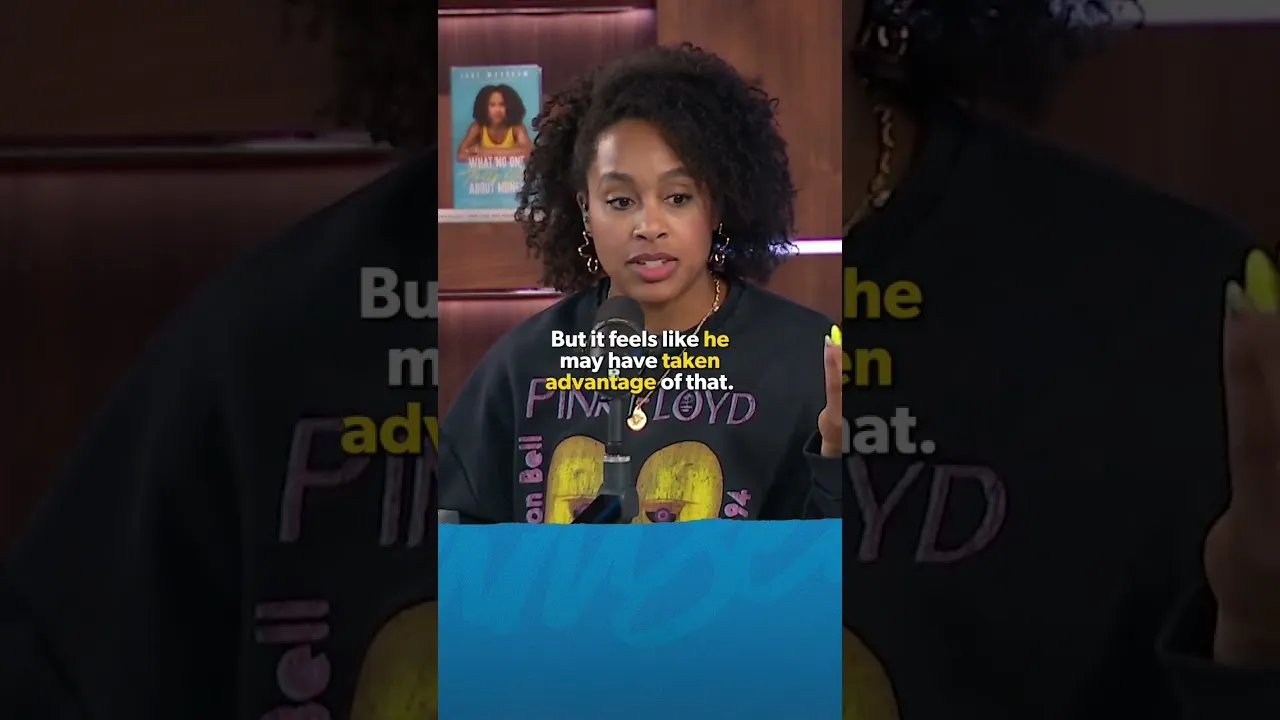

The child’s perspective suggests a feeling of being taken advantage of, stating, “I’m just telling you as a person who’s listening on the other side. There was an imbalance of knowledge here. You have a grown man who you trust who is a lawyer who is giving you a paper to sign and you just go, ‘Okay.’ And I sign it.” This sentiment underscores a significant power dynamic at play, where trust in a parental figure, coupled with their professional expertise as a lawyer, may have led to an unwitting commitment.

Understanding 529 Plans

529 plans are designed to help families save for future education costs. Contributions grow tax-deferred, and withdrawals are tax-free when used for qualified education expenses, such as tuition, fees, books, and room and board. While the beneficiary of a 529 plan is typically the student, the account owner (usually a parent or guardian) has control over the funds. This dispute brings to light a potential gray area where the intent behind the withdrawal and subsequent parental expectations diverge from the typical understanding of 529 plan usage.

Navigating the Obligation

The child’s primary question revolves around the nature of the funds: “Can my 529 just be for my education, which is what it’s intended to be for?” This question points to a fundamental misunderstanding or misrepresentation of the terms under which the funds were accessed. The expectation of repayment suggests that the parents may have viewed the 529 funds as a personal loan to their child, rather than an investment in their education.

When presented with the possibility of offering some money or meeting in the middle, the child expresses openness: “Maybe. Yeah. Yeah.” This suggests a willingness to find a resolution, possibly by understanding the extent of the parents’ contributions and finding a compromise.

Seeking Legal Clarity

A crucial piece of advice offered in this situation is to seek independent legal counsel. The transcript suggests:

- Consult an Attorney: “I would honestly, if you want to consult with your own attorney and say, ‘Hey, what is actually in this? Does this actually hold up? Should I actually be worried? What is actually my obligation based on what I signed?'”

- Understand the Document: The purpose of consulting an attorney would be to gain clarity on the legal standing of the signed document and the child’s actual financial obligations.

- Assess the Agreement: Determining the enforceability and true meaning of the agreement is paramount.

This step is vital to understand whether the child is legally bound to repay the funds and under what terms. The involvement of a lawyer in presenting the initial document complicates matters, as it implies a level of legal formality that could be binding.

What Investors Should Know

This case, while specific to a family dynamic, touches upon broader themes relevant to financial planning and family wealth transfer:

- Clarity in Agreements: Any financial assistance, especially involving funds designated for specific purposes like education, should be clearly documented. Ambiguity can lead to disputes, particularly when family members are involved.

- Purpose of Savings Vehicles: It’s essential to understand the rules and intended uses of financial products like 529 plans. While flexible, they are designed for educational expenses, and deviations may have tax implications or lead to misunderstandings.

- Power Dynamics: In family financial matters, inherent power imbalances (due to age, knowledge, or legal expertise) can lead to situations where one party feels disadvantaged. Open communication and transparency are key to mitigating this.

- Seeking Independent Advice: When significant financial commitments or disputes arise, consulting with independent legal and financial professionals is crucial to protect one’s interests and ensure a clear understanding of obligations.

The long-term implications for the individuals involved will depend on the clarity of the signed document and their ability to reach an amicable resolution, potentially with the guidance of legal professionals. For families utilizing 529 plans, this situation serves as a cautionary tale about ensuring clear communication and understanding regarding the use and expectations associated with these valuable educational savings tools.

Source: Her Parents Expect Her to Pay Back Money Her "Student Loan" (YouTube)