Small Savings Yield Millions: The Power of Incremental Investing

A seemingly small increase in savings can lead to a dramatically larger nest egg over time. New analysis highlights how boosting savings rates, even by a few percentage points, can result in millions more dollars by retirement. This underscores the significant impact of consistent, incremental financial habits.

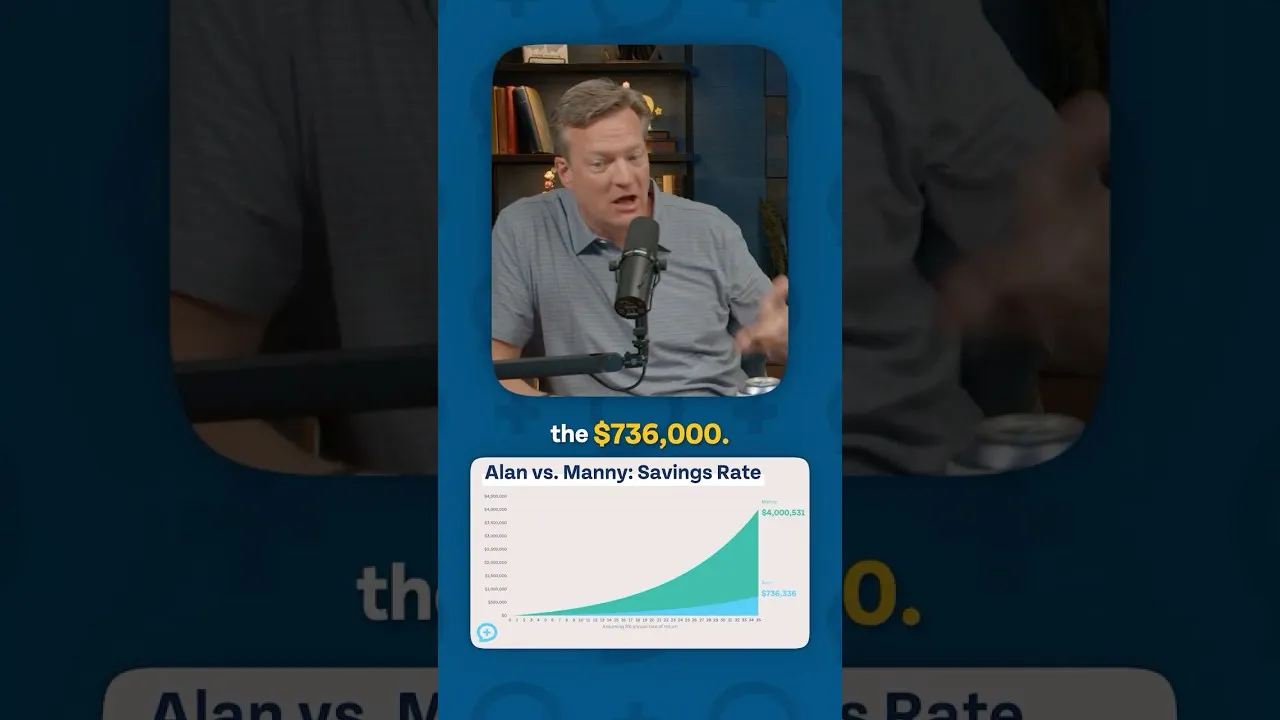

Consider two hypothetical savers, both starting at age 30. One, dubbed ‘Average Allen,’ saves 4.6% of their income. The other, ‘Manny the Mute,’ saves a more aggressive 25%. The results by retirement age are starkly different.

Manny, with the higher savings rate, is projected to accumulate close to $4 million. This impressive sum comes from consistently setting aside a quarter of his earnings. Meanwhile, Average Allen, representing a typical American saver, falls far short of even a modest goal. Allen’s 4.6% savings rate doesn’t even reach $736,000 by retirement.

The analysis further reveals a concerning trend: many typical Americans struggle to maintain even these lower savings rates consistently. The path from saving a small percentage to a large one can seem daunting. However, the key takeaway is that even small, manageable increases can make a substantial difference.

The Power of Small Steps

For individuals finding it difficult to jump from a 4.6% savings rate to 25%, the advice is to start small and build momentum. Instead of aiming for a huge leap, consider a gradual increase. For example, moving from 4.6% to 5.6% is a manageable step. The next goal could be increasing it to 6.6%.

This strategy of incremental saving is powerful because it makes the goal feel achievable. It allows individuals to adjust their budgets and spending habits without feeling overwhelmed. Over years and decades, these small percentage point increases compound significantly, thanks to the magic of compound interest.

Compound interest is like a snowball rolling downhill. It not only grows with the money you add but also earns returns on the returns it has already generated. This effect is amplified the longer your money is invested, making early and consistent saving crucial.

Market Context and Investor Implications

The S&P 500 index, a broad measure of U.S. stock market performance, has historically provided average annual returns of around 10%. While individual results vary, this long-term trend highlights the potential growth available through investing. Saving is the first step; investing that saved money is how it grows.

For the average saver, the challenge is often not just saving but also investing wisely. Many retirement accounts, like 401(k)s and IRAs, offer investment options. Understanding these options, such as low-cost index funds or target-date funds, can help maximize returns.

The difference between Manny’s $4 million and Allen’s sub-$736,000 is a testament to the power of both a higher savings rate and the compounding effect of investment returns over a long period, typically 30-40 years from age 30 to 60 or 70.

What Investors Should Know

The core message is that significant wealth accumulation is within reach for more people than currently achieve it. It requires a disciplined approach to saving and a commitment to letting investments grow over time.

- Start Early: The earlier you begin saving, the more time compound interest has to work its magic.

- Increase Gradually: Don’t be discouraged by large savings targets. Focus on small, consistent increases.

- Automate Savings: Set up automatic transfers from your checking account to your savings or investment accounts. This removes the temptation to spend the money.

- Invest Consistently: Once saved, ensure the money is invested in a diversified portfolio aligned with your risk tolerance and time horizon.

- Review and Adjust: Periodically review your savings rate and investment performance. Adjust your strategy as needed, especially after major life events like salary increases.

The gap between Average Allen and Manny the Mute illustrates a critical financial principle: consistent, slightly higher savings, coupled with the long-term growth of investments, can lead to vastly different financial futures. The journey to financial security is often paved with small, consistent steps rather than giant leaps.

Source: The Small Saving Change That Adds Up Big (YouTube)